kfoldCV.ridge <- function(K, lambdas, dataset, responseVar){

m <- length(lambdas)

#idx is a shuffled vector of row numbers

idx <- sample(1:nrow(dataset))

#folds partitions the row indices

folds <- split(idx, as.factor(1:K))

#an empty data frame to store the results of each validation

results <- data.frame(fold = rep(1:K, rep(m,K)),

model = rep(1:m, K),

error = 0)

for(k in 1:K){

#split the data into training and testing sets

training <- dataset[-folds[[k]],]

testing <- dataset[folds[[k]],]

#go through each model and estimate MSE

ridge_models <- lm.ridge(reformulate(".",responseVar), training, lambda=lambdas);

for(f in 1:m){

coeff <- coef(ridge_models)[f,]

Y <- testing[,c(responseVar)]

X <- cbind( 1, testing[,names(dataset) != responseVar])

Y.hat <- as.numeric(coeff) %*% as.matrix(t(X))

#calculate the average squared error on the testing data

results[results$fold == k & results$model == f, "error"] <- mean((Y-Y.hat)^2)

}

}

#aggregate over each model, averaging the error

aggregated <- aggregate(error~model, data=results, FUN="mean")

#produces a simple line & dot plot

plot(error ~ sqrt(lambdas), type="b", data=aggregated, ylab="MSE")

# lines(error ~ model, data=aggregated)

print(which(aggregated$error == min(aggregated$error)))

print(lambdas[[which(aggregated$error == min(aggregated$error))]])

return(aggregated)

}38 R11: Ridge and Lasso

38.1 K Fold Validation for Ridge Regression

38.2 Ridge Regression

library(MASS);Warning: package 'MASS' was built under R version 4.2.3lambda_vals <- seq(0,10,1)^2; # Choose lambdas to try.

# lm.ridge needs:

# 1) a model (mpg~. says to model mpg as an intercept

# plus a coefficient for every other variable in the data frame)

# 2) a data set (mtcars, of course)

# 3) a value for lambda. lambda=0 is the default,

# and recovers classic linear regression.

# But we can also pass a whole vector of lambdas, like we are about to do,

# and lm.ridge will fit a separate model for each.

# See ?lm.ridge for details.

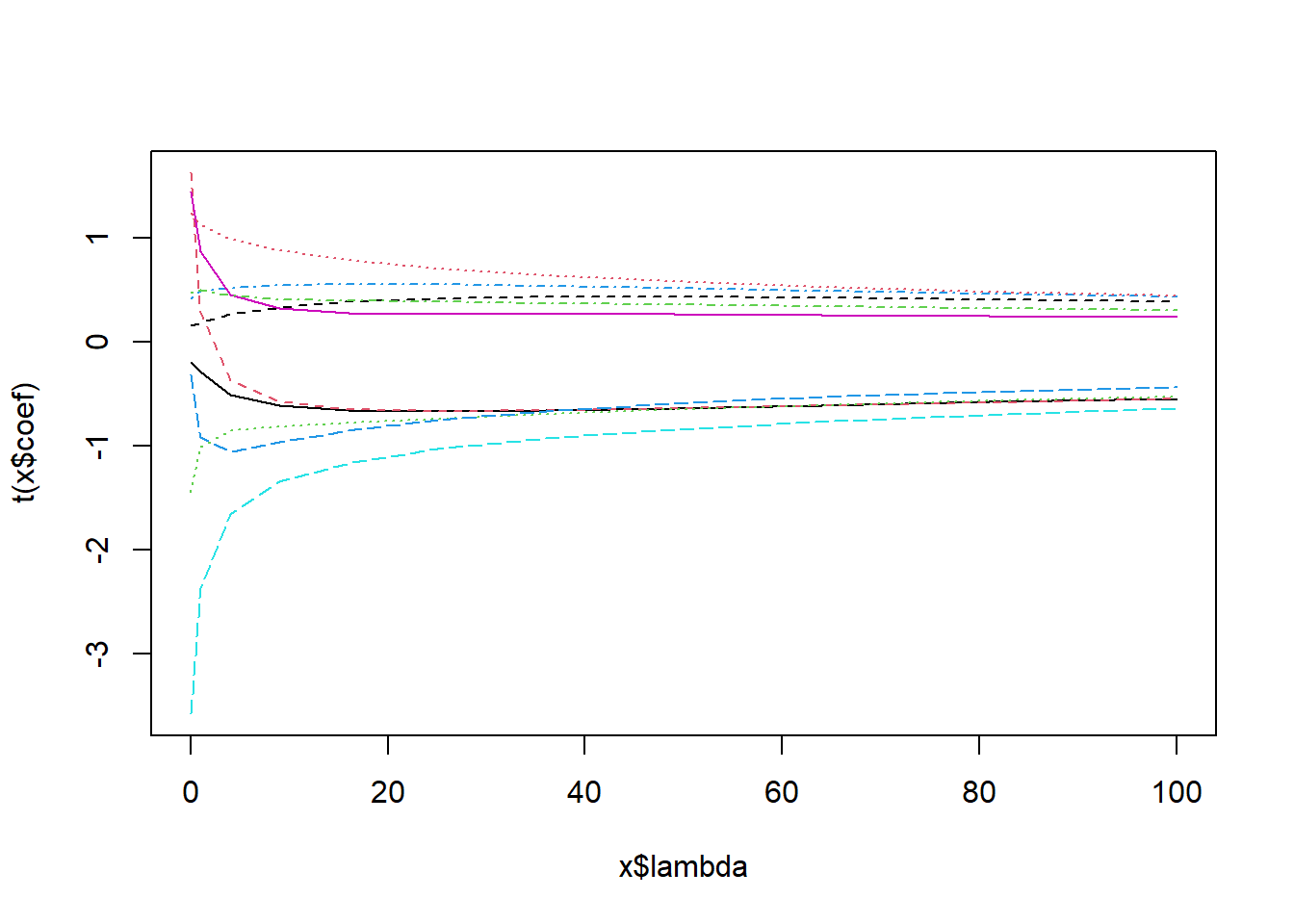

ridge_models <- lm.ridge(mpg~., mtcars, lambda=lambda_vals);

# Naively plotting this object shows us how the different coefficients

# change as lambda changes.

plot( ridge_models );

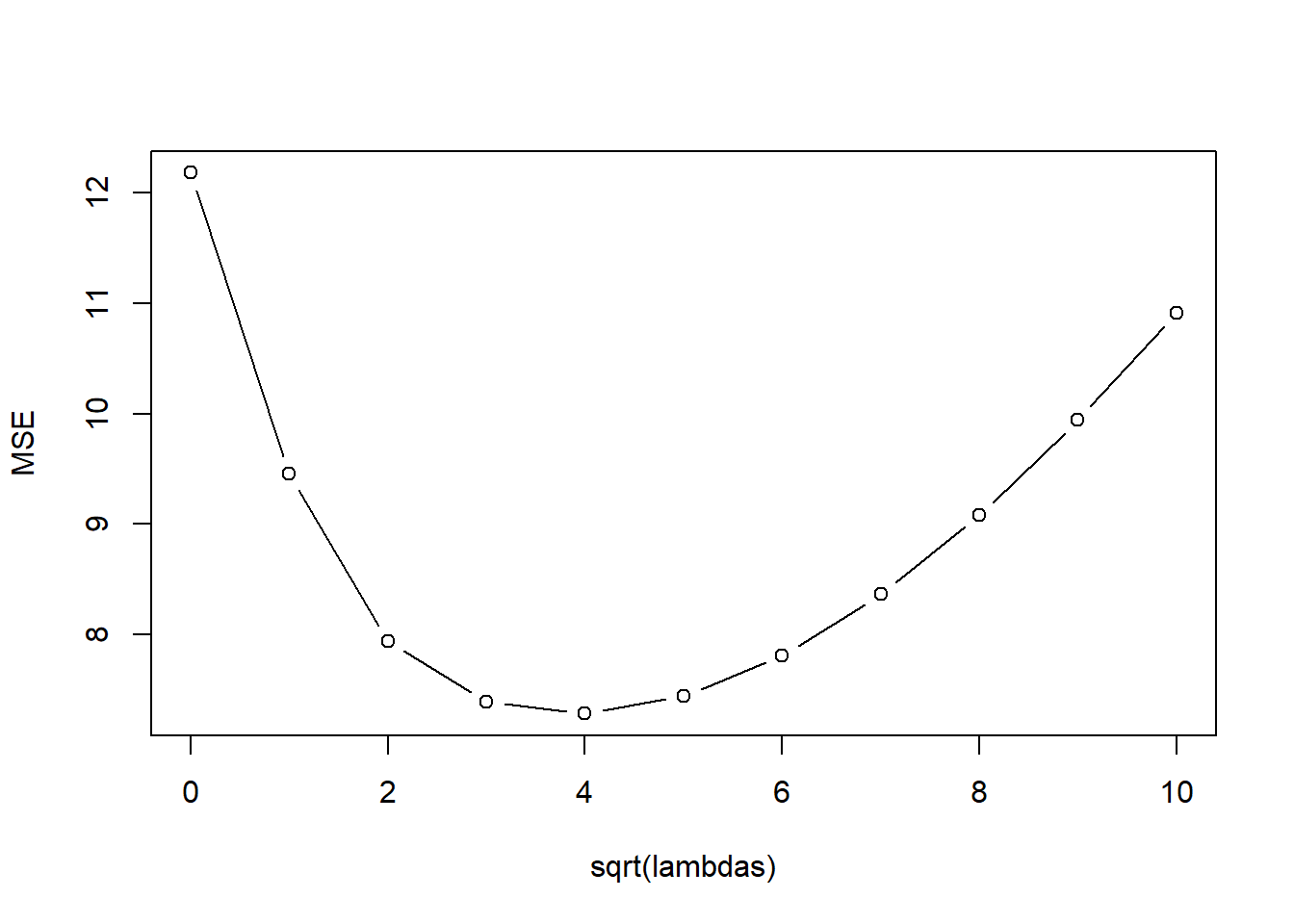

kfoldCV.ridge(32, lambda_vals, mtcars, "mpg")

[1] 5

[1] 16 model error

1 1 12.181558

2 2 9.452096

3 3 7.936502

4 4 7.393522

5 5 7.283203

6 6 7.441021

7 7 7.809000

8 8 8.361948

9 9 9.080131

10 10 9.940278

11 11 10.914771ridge_models$coef 0 1 4 9 16 25

cyl -0.1958895 -0.2854708 -0.5066139 -0.6161717 -0.6591445 -0.6683601

disp 1.6267230 0.2846046 -0.3725236 -0.5766167 -0.6490976 -0.6685263

hp -1.4496794 -1.0078499 -0.8528542 -0.8129980 -0.7775318 -0.7375242

drat 0.4142235 0.4865947 0.5232729 0.5453579 0.5549330 0.5519234

wt -3.5780149 -2.3702010 -1.6545051 -1.3466497 -1.1634754 -1.0318544

qsec 1.4440470 0.8663632 0.4563819 0.3199939 0.2816562 0.2727392

vs 0.1576353 0.1858566 0.2665591 0.3379935 0.3882118 0.4182555

am 1.2377648 1.1337179 0.9930509 0.8779217 0.7836540 0.7053996

gear 0.4759507 0.4979561 0.4415798 0.4078556 0.3938022 0.3845387

carb -0.3170292 -0.9153711 -1.0545303 -0.9681697 -0.8536815 -0.7501713

36 49 64 81 100

cyl -0.6584602 -0.6371174 -0.6089930 -0.5771490 -0.5436589

disp -0.6618424 -0.6410597 -0.6125306 -0.5799961 -0.5457984

hp -0.6949141 -0.6515838 -0.6087390 -0.5671623 -0.5273766

drat 0.5389018 0.5188717 0.4944121 0.4675133 0.4396305

wt -0.9277904 -0.8409367 -0.7659920 -0.6999756 -0.6410990

qsec 0.2700141 0.2662930 0.2599270 0.2510841 0.2404236

vs 0.4315668 0.4322241 0.4239420 0.4097144 0.3918058

am 0.6390688 0.5816137 0.5309703 0.4857926 0.4451943

gear 0.3737460 0.3599879 0.3436658 0.3256615 0.3068348

carb -0.6631350 -0.5906396 -0.5296824 -0.4777057 -0.432798738.3 Ridge Regression With Standardized Data

One problem that we will encounter with Ridge regression (and LASSO) is that it assumes large betas are large because the predictor is important. This is not necessarily true - it could be due to the units of the variable.

Consider a model of mpg based on weight in pounds.

lm(mpg~ I(1000*wt), data=mtcars)

Call:

lm(formula = mpg ~ I(1000 * wt), data = mtcars)

Coefficients:

(Intercept) I(1000 * wt)

37.285126 -0.005344 When we convert weight to pounds (multiply by 1000) then the coefficient is -.005. But if we have wt in 1000s of pounds

lm(mpg~ wt, data=mtcars)

Call:

lm(formula = mpg ~ wt, data = mtcars)

Coefficients:

(Intercept) wt

37.285 -5.344 The coefficient is 1000x as large! For this reason it is a good idea to standardize your data before you apply a shrinkage method. Standardized data requires subtracting the mean and dividing by standard deviation (of that column): \[ Z_{i,j} = \frac{X_{i,j} - \bar{X}_j}{S_{j}}\] No need to standardize the response variable.

mtcars.std <- mtcars

#let's standardize the quantitative predictors

stdcols <- c("cyl","disp","hp","drat","wt","qsec","gear","carb")

for(col in stdcols){

xbar <- mean(mtcars.std[,col])

sd <- sd(mtcars.std[,col])

mtcars.std[,col] <- (mtcars.std[,col]-xbar)/sd

}

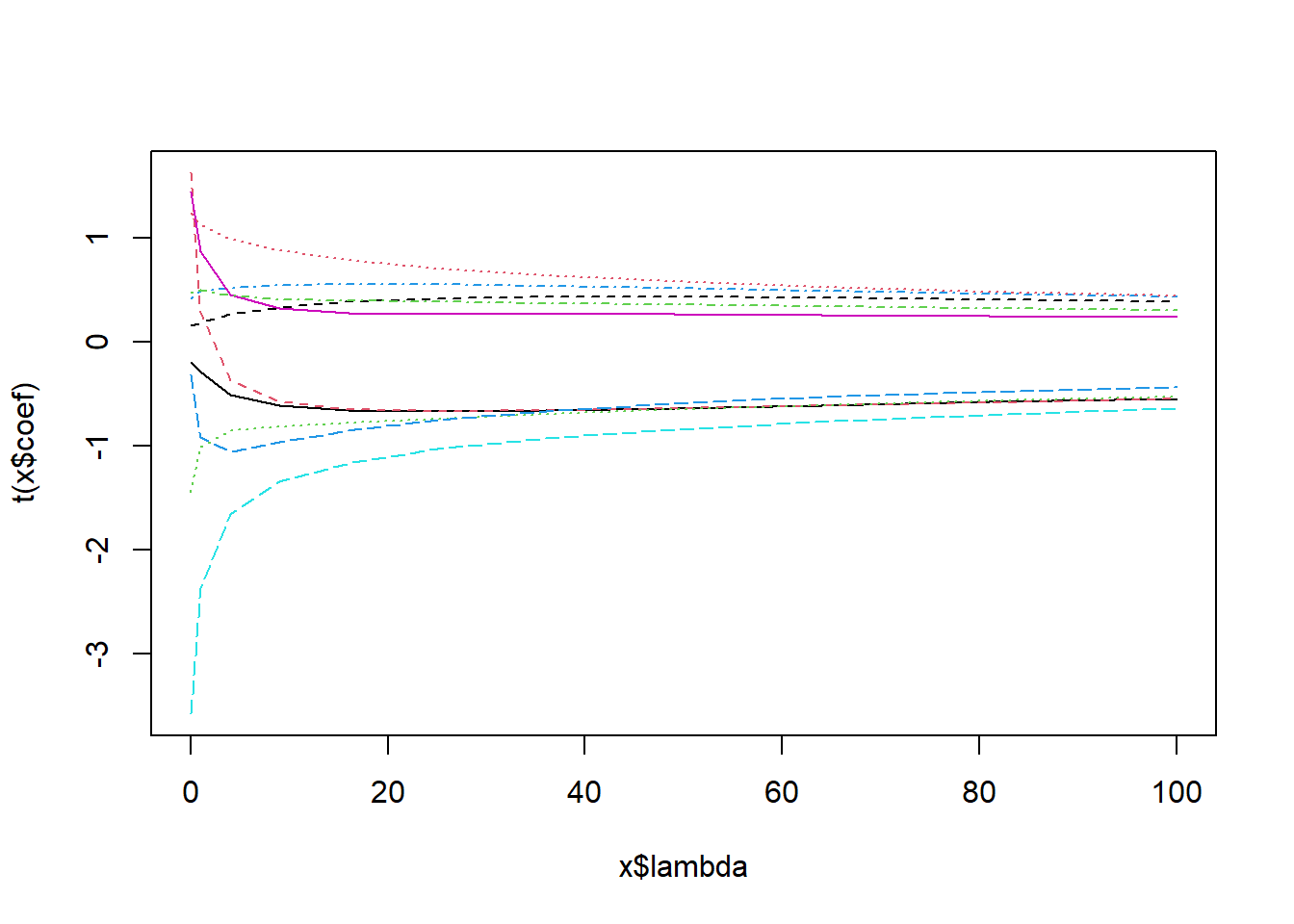

lambda_vals <- seq(0,10,1)^2; # Choose lambdas to try.

ridge_models <- lm.ridge(mpg~., mtcars.std, lambda=lambda_vals);

plot( ridge_models );

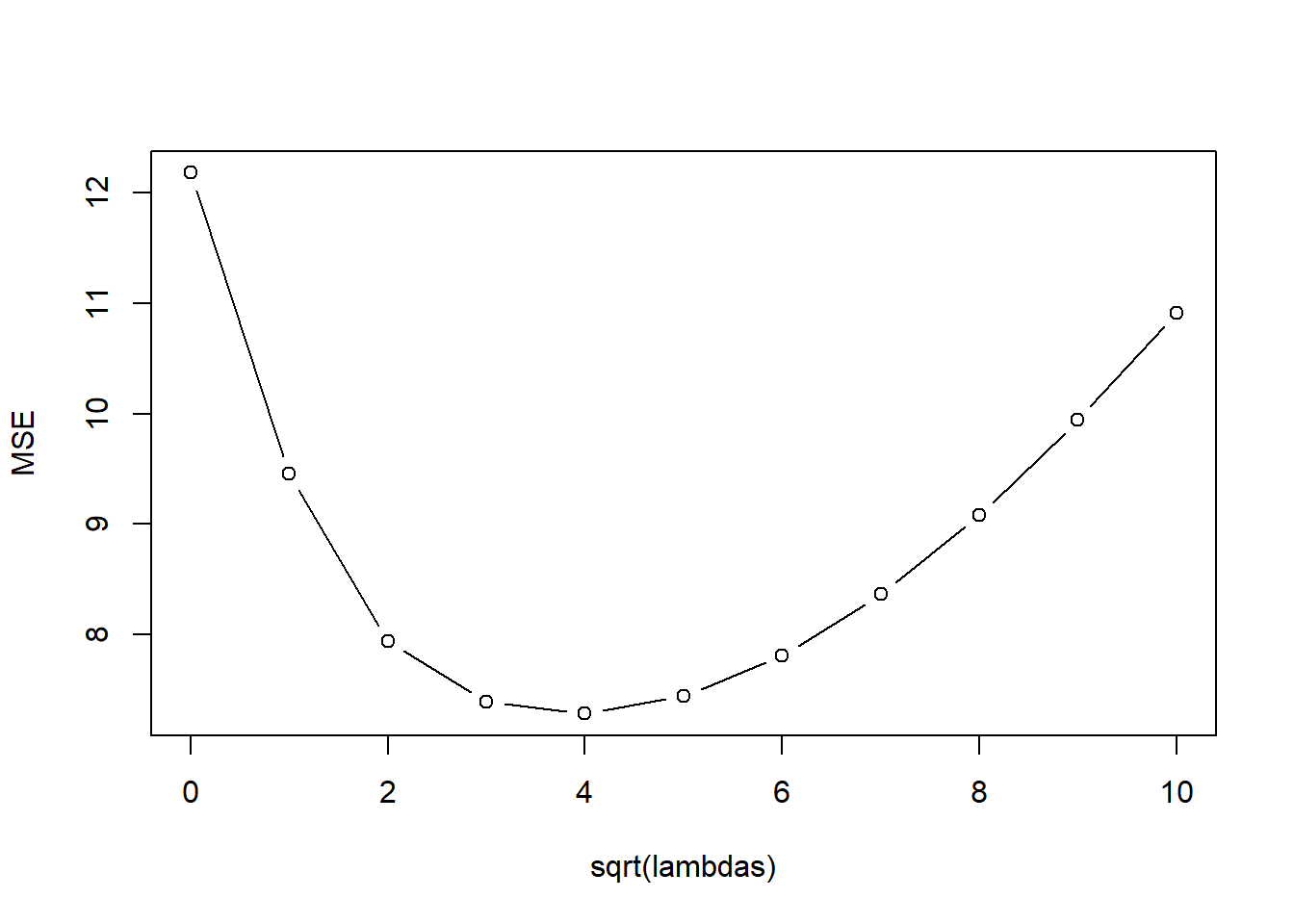

kfoldCV.ridge(32, lambda_vals, mtcars.std, "mpg")

[1] 5

[1] 16 model error

1 1 12.181558

2 2 9.452096

3 3 7.936502

4 4 7.393522

5 5 7.283203

6 6 7.441021

7 7 7.809000

8 8 8.361948

9 9 9.080131

10 10 9.940278

11 11 10.91477138.4 LASSO Regression

library(glmnet)Loading required package: MatrixLoaded glmnet 4.1-10kfoldCV.LASSO <- function(K, lambdas, dataset, responseVar){

m <- length(lambdas)

#idx is a shuffled vector of row numbers

idx <- sample(1:nrow(dataset))

#folds partitions the row indices

folds <- split(idx, as.factor(1:K))

#an empty data frame to store the results of each validation

results <- data.frame(fold = rep(1:K, rep(m,K)),

model = rep(1:m, K),

error = 0)

for(k in 1:K){

#split the data into training and testing sets

training <- dataset[-folds[[k]],]

testing <- dataset[folds[[k]],]

#go through each model and estimate MSE

for(f in 1:m){

mtc_lasso_lambda <- glmnet(training[,names(dataset) != responseVar], training[,c(responseVar)], alpha = 1, lambda=lambdas[f]);

coeffs <- as.vector(coef(mtc_lasso_lambda))

y.mtc.predict <- coeffs %*% t(cbind(1,testing[,names(dataset) != responseVar]))

results[results$fold == k & results$model == f, "error"] <- mean((y.mtc.predict-testing[,c(responseVar)])^2)

}

}

#aggregate over each model, averaging the error

aggregated <- aggregate(error~model, data=results, FUN="mean")

#produces a simple line & dot plot

plot(error ~ lambdas, type="b", data=aggregated, ylab="MSE")

# print(which(aggregated$error == min(aggregated$error)))

print(paste("best lambdas:", paste(lambdas[which(aggregated$error == min(aggregated$error))], collapse=",")))

return(aggregated)

}#LASSO mpg on mtcars

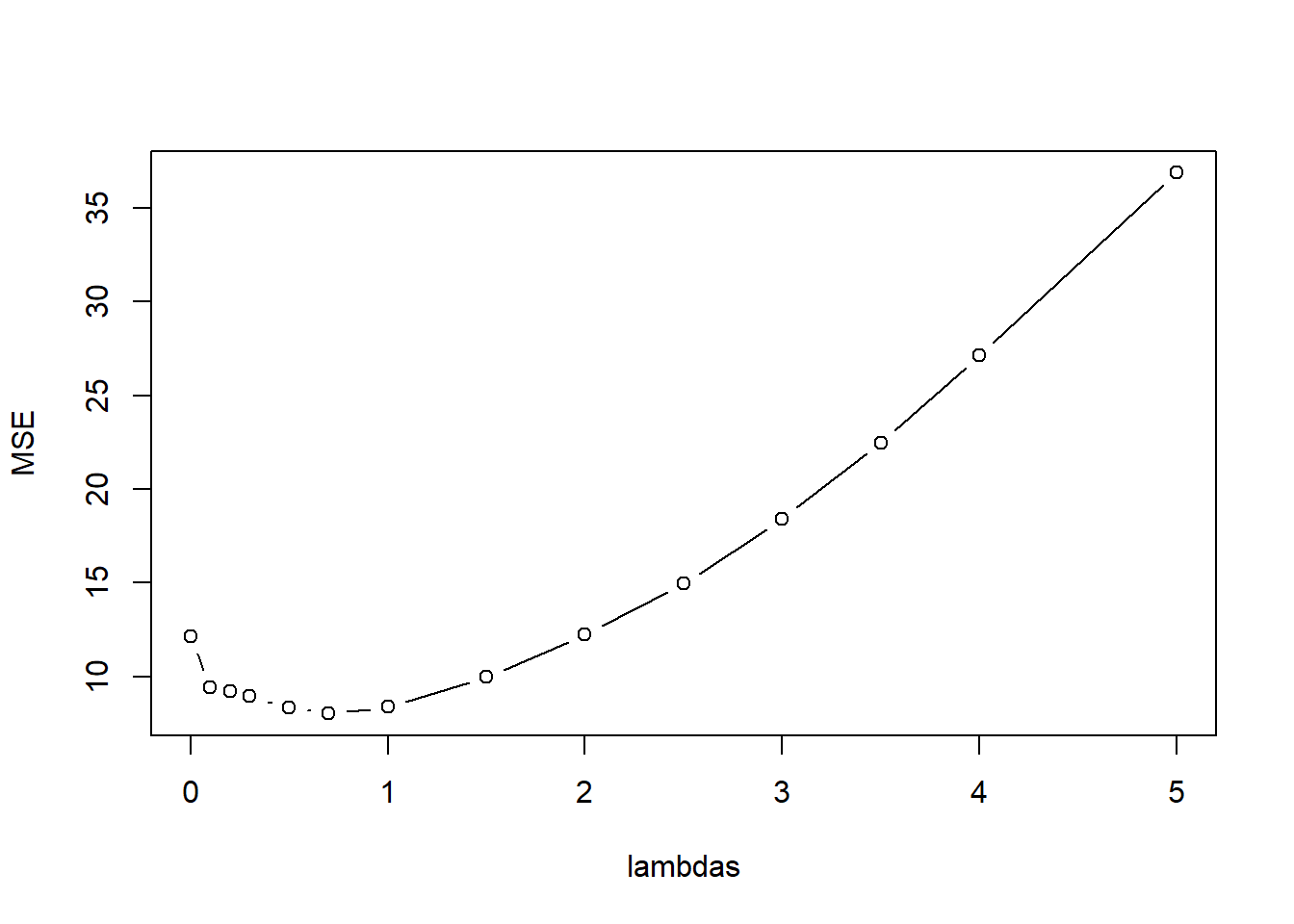

lambda_vals <- c(0,.1,.2,.3,.5,.7, 1, 1.5, 2, 2.5, 3, 3.5, 4, 5)

kfoldCV.LASSO(32, lambda_vals, mtcars.std, "mpg")

[1] "best lambdas: 0.7" model error

1 1 12.139522

2 2 9.401635

3 3 9.208783

4 4 8.945935

5 5 8.314812

6 6 8.013806

7 7 8.357635

8 8 9.960995

9 9 12.241522

10 10 14.956380

11 11 18.398062

12 12 22.475571

13 13 27.129122

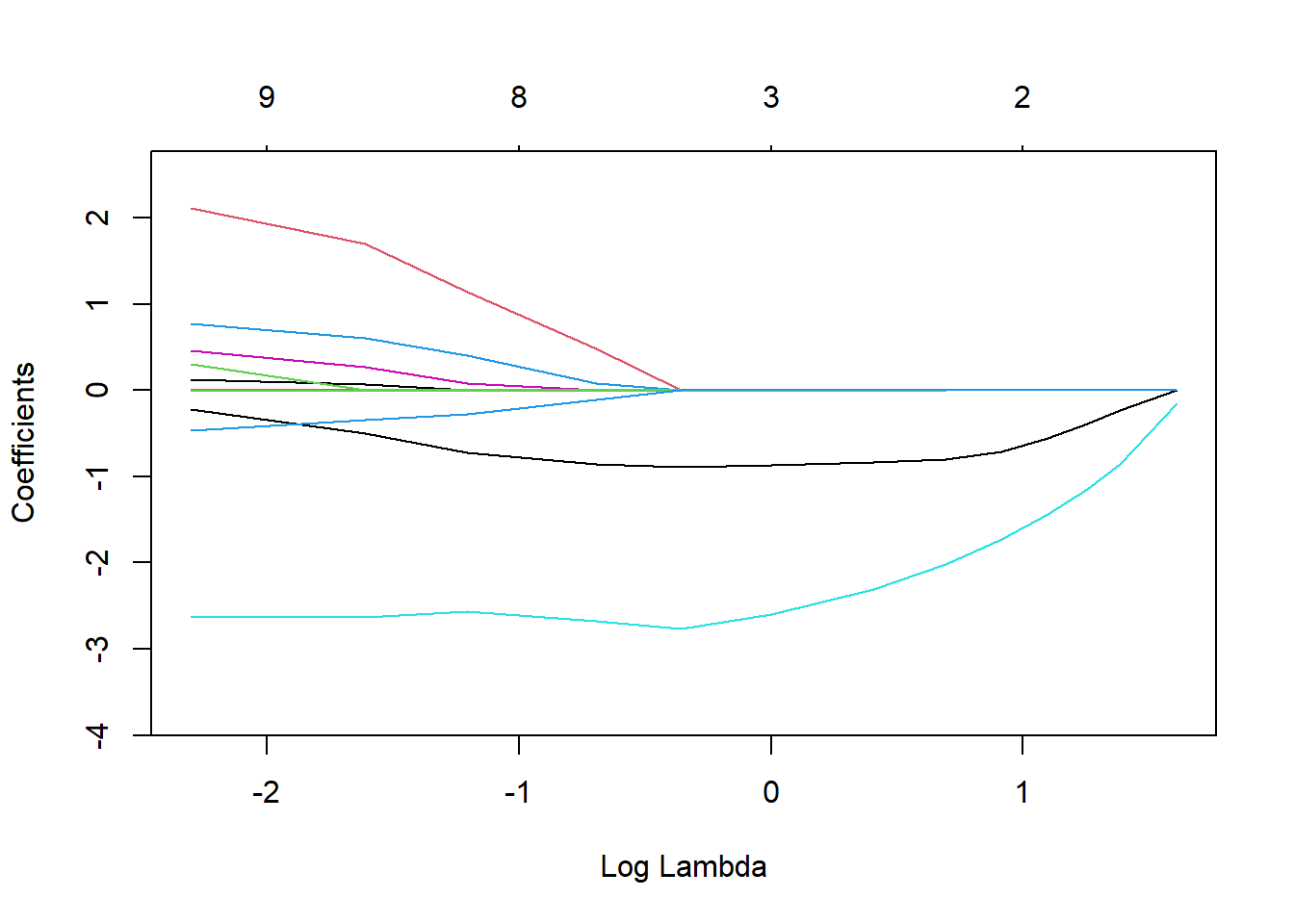

14 14 36.870189LASSO.fits <- glmnet(mtcars[,-1], mtcars[,1], alpha=1, lambda=lambda_vals)

plot(LASSO.fits, label=TRUE, xvar="lambda")

LASSO_coeff<- t(coef(LASSO.fits))

#colnames(LASSO_coeff) <- c("intercept",names(mtcars)[-1])

LASSO_coeff14 x 11 sparse Matrix of class "dgCMatrix" [[ suppressing 11 column names '(Intercept)', 'cyl', 'disp' ... ]]

s0 20.58164 . . . . -0.1526208

s1 24.29182 -0.2320135 . . . -0.8596190

s2 26.21643 -0.3916771 . . . -1.1507654

s3 28.14090 -0.5512556 . . . -1.4420334

s4 30.06537 -0.7108337 . . . -1.7333021

s5 31.87369 -0.8000158 . -0.002226427 . -2.0223414

s6 33.59349 -0.8355844 . -0.006175353 . -2.3084431

s7 35.31356 -0.8713207 . -0.010120873 . -2.5944626

s8 36.34612 -0.8930789 . -0.012481712 . -2.7659212

s9 35.87185 -0.8564098 . -0.014070252 0.07915497 -2.6716570

s10 32.27520 -0.7185199 . -0.014111007 0.40765131 -2.5704279

s11 26.92701 -0.5030523 . -0.013211244 0.60633782 -2.6290418

s12 20.12195 -0.2164116 . -0.013112947 0.77468208 -2.6356369

s13 12.32700 -0.1194297 0.01369736 -0.021693022 0.78186836 -3.7504495

s0 . . . . .

s1 . . . . .

s2 . . . . .

s3 . . . . .

s4 . . . . .

s5 . . . . .

s6 . . . . .

s7 . . . . .

s8 . . . . .

s9 . . 0.4869054 . -0.1085726

s10 0.08195105 0.003182207 1.1364003 . -0.2812566

s11 0.26537365 0.068664832 1.6929202 . -0.3422762

s12 0.45898572 0.123968843 2.1142688 0.3046746 -0.4637967

s13 0.82638838 0.316450552 2.5192826 0.6476344 -0.185440038.5 Boston Dataset Example

data("Boston")

library(glmnet)

#Standardize Variables

Boston.std <- Boston

for(i in 1:(ncol(Boston.std)-1)){

Boston.std[,i] <- (Boston.std[,i]-mean(Boston.std[,i]))/sd(Boston.std[,i])

}

lambda_vals <- seq(0,5,length.out=10)^2; # Choose lambdas to try.

ridge_models <- lm.ridge(medv ~ . , Boston.std, lambda=lambda_vals);

plot( ridge_models );

kfoldCV.ridge(4, lambda_vals, Boston.std, "medv")

[1] 4

[1] 2.777778 model error

1 1 23.22624

2 2 23.22228

3 3 23.21316

4 4 23.20575

5 5 23.20800

6 6 23.22627

7 7 23.26433

8 8 23.32364

9 9 23.40416

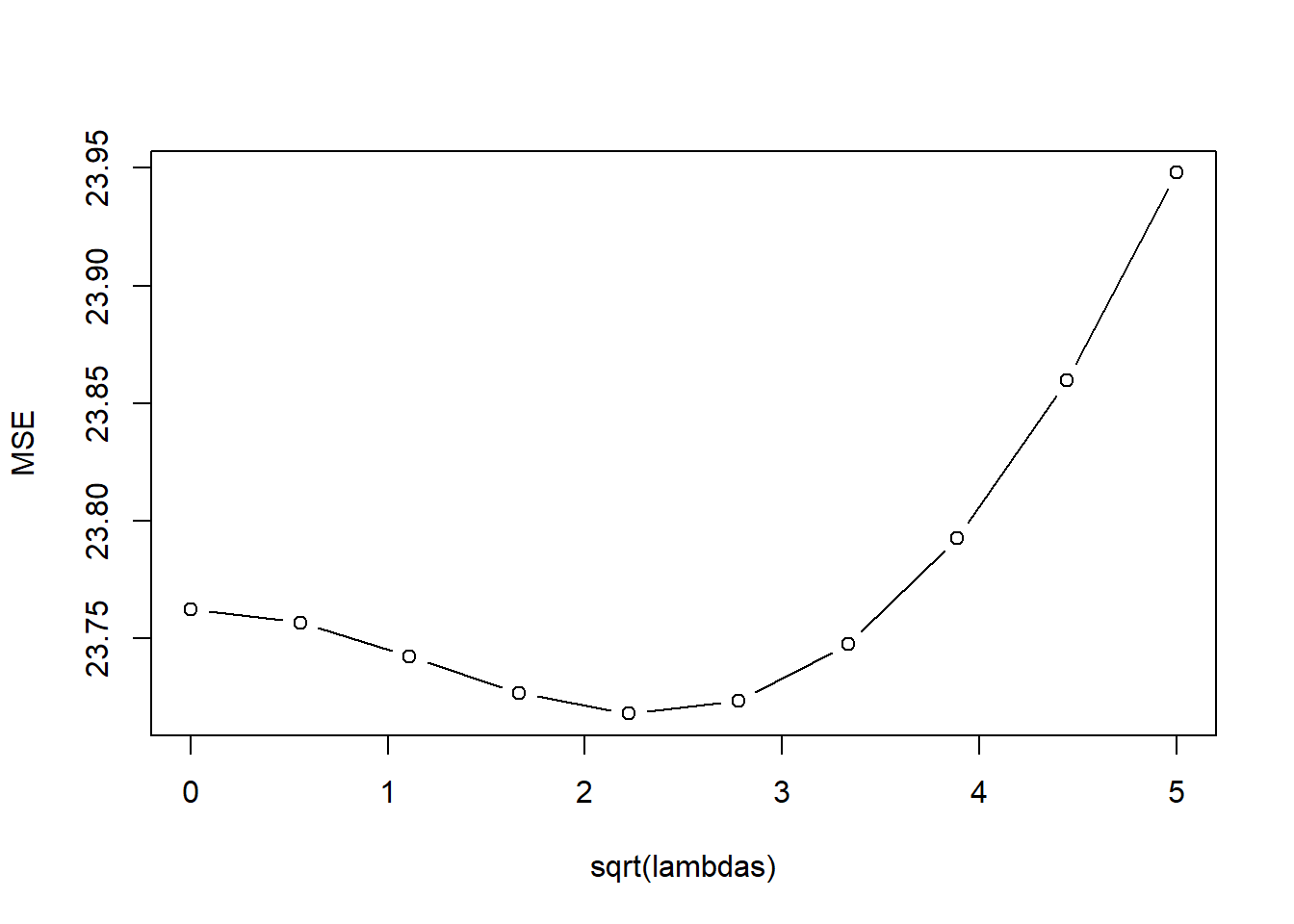

10 10 23.50516#LASSO

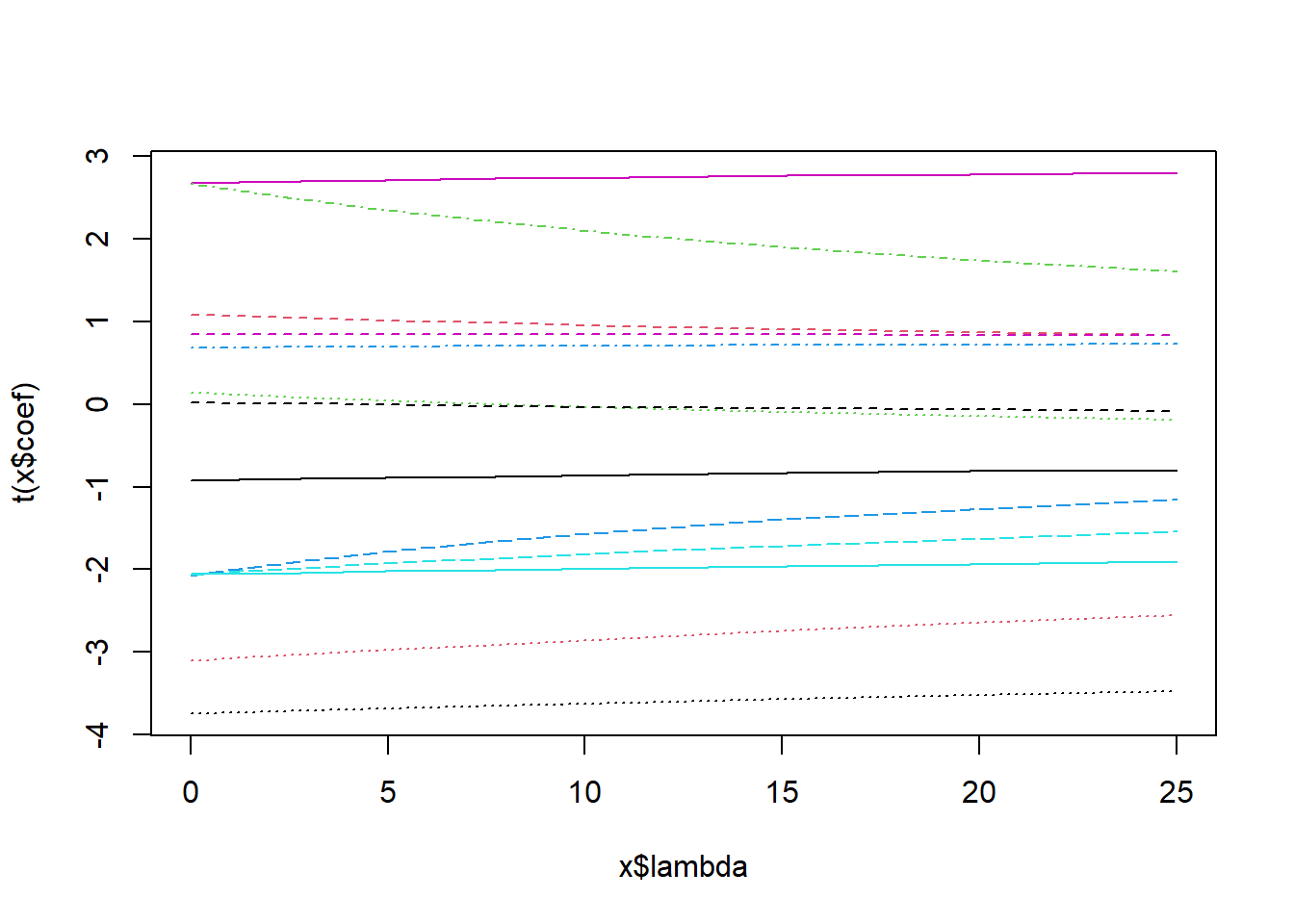

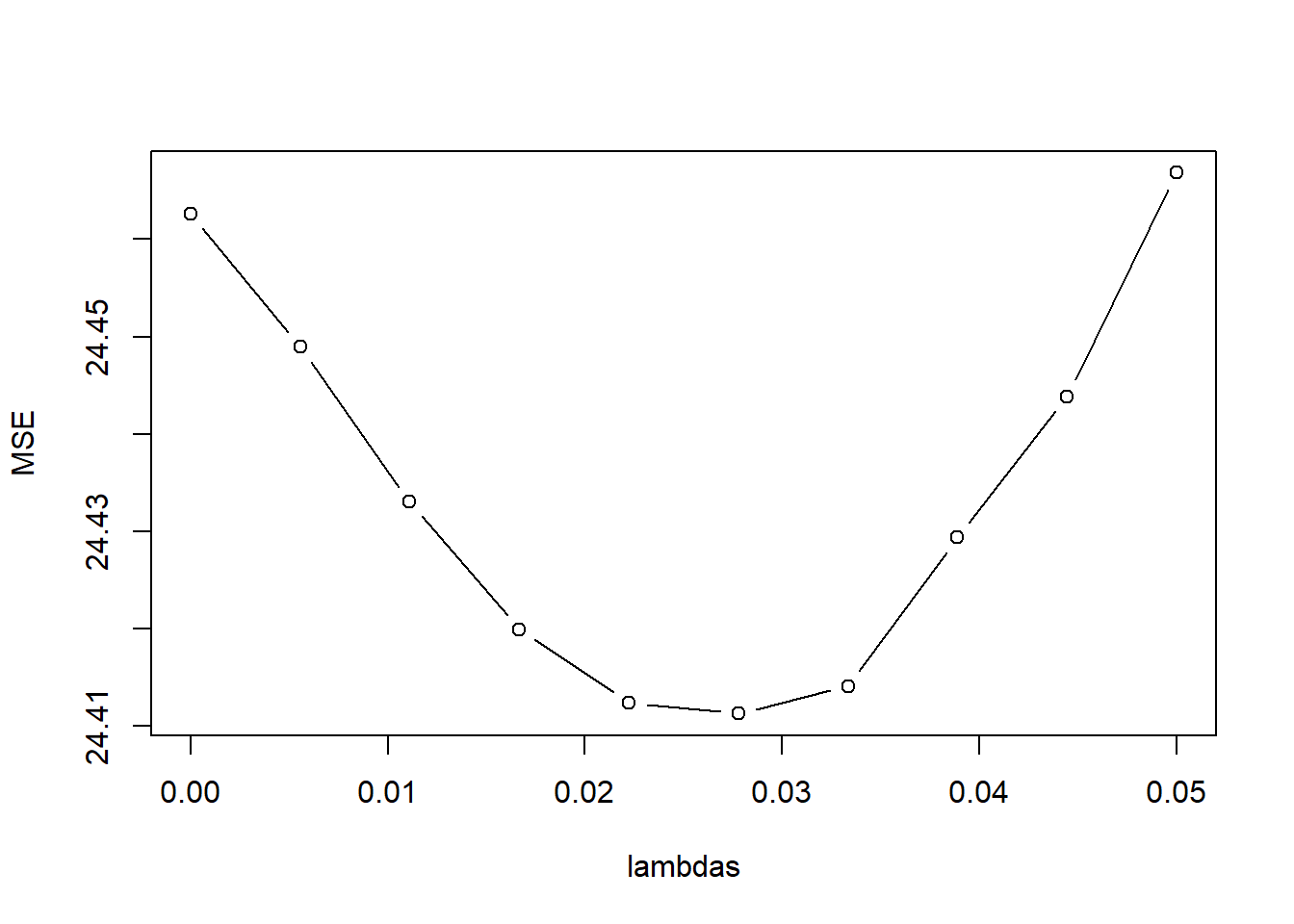

lambda_vals <- seq(0,.05,length.out=10)

LASSO.fits <- glmnet(Boston.std[,names(Boston.std)!="medv"], Boston[,"medv"], alpha=1, lambda=lambda_vals)

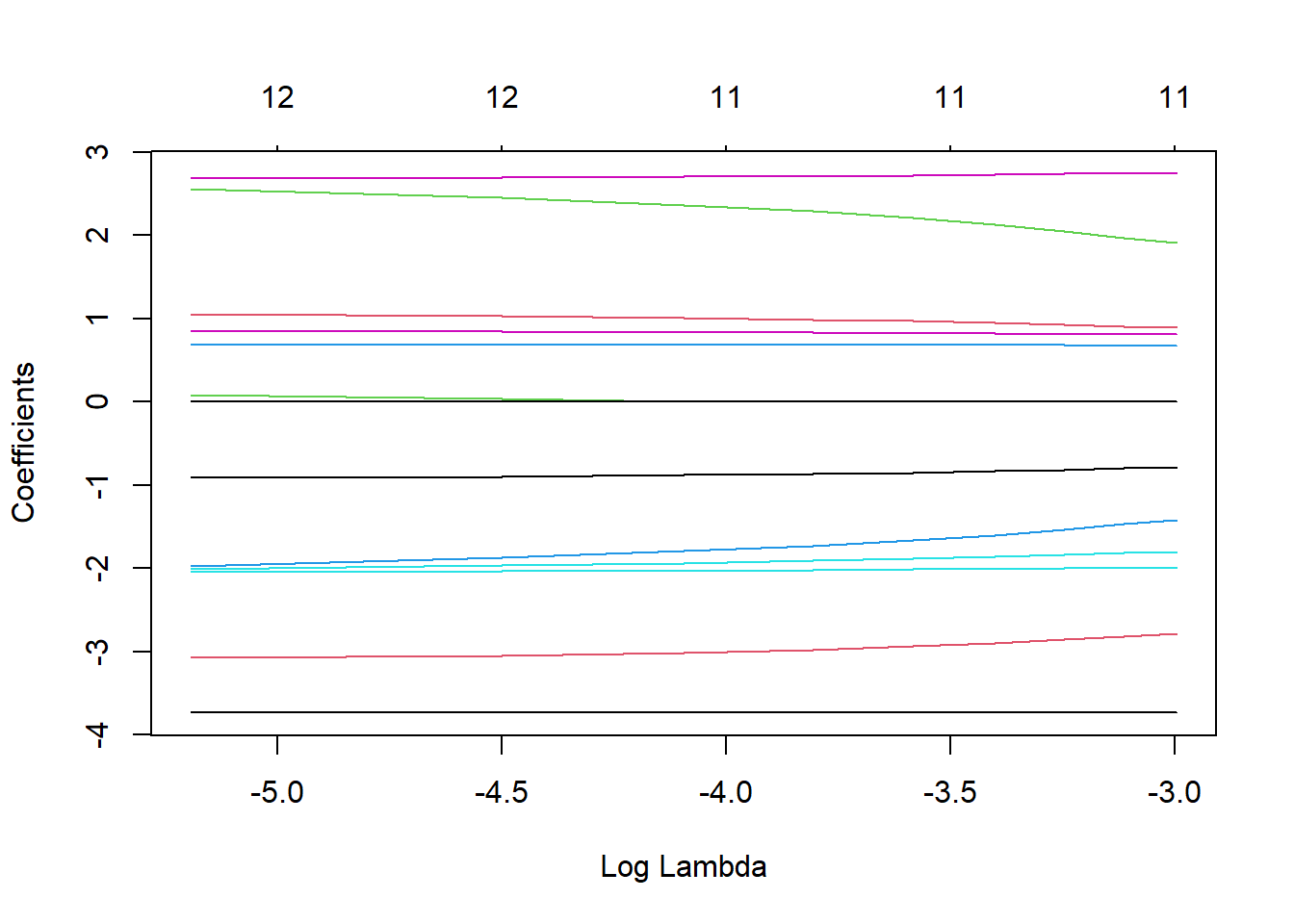

plot(LASSO.fits, label=TRUE, xvar="lambda")

kfoldCV.LASSO(10, lambda_vals, Boston.std, "medv")Warning in split.default(idx, as.factor(1:K)): data length is not a multiple of

split variable

[1] "best lambdas: 0.0166666666666667" model error

1 1 23.80285

2 2 23.79381

3 3 23.78668

4 4 23.78288

5 5 23.78492

6 6 23.79383

7 7 23.80548

8 8 23.82536

9 9 23.85166

10 10 23.88365resultsTable <- t(as.matrix(coef(LASSO.fits)))

row.names(resultsTable) <- sort(lambda_vals,decreasing=TRUE)

round(resultsTable,3) (Intercept) crim zn indus chas nox rm age

0.05 22.533 -0.783 0.891 0.000 0.674 -1.799 2.747 0.000

0.0444444444444444 22.533 -0.799 0.907 0.000 0.677 -1.814 2.744 0.000

0.0388888888888889 22.533 -0.816 0.927 0.000 0.678 -1.838 2.735 0.000

0.0333333333333333 22.533 -0.832 0.947 0.000 0.680 -1.863 2.726 0.000

0.0277777777777778 22.533 -0.849 0.967 0.000 0.682 -1.887 2.718 0.000

0.0222222222222222 22.533 -0.865 0.987 0.000 0.684 -1.911 2.708 0.000

0.0166666666666667 22.533 -0.882 1.007 0.000 0.686 -1.935 2.700 0.000

0.0111111111111111 22.533 -0.898 1.029 0.031 0.686 -1.968 2.693 0.000

0.00555555555555556 22.533 -0.913 1.053 0.084 0.684 -2.006 2.687 0.000

0 22.533 -0.928 1.078 0.138 0.683 -2.049 2.680 0.017

dis rad tax ptratio black lstat

0.05 -2.789 1.914 -1.424 -1.988 0.806 -3.732

0.0444444444444444 -2.818 1.971 -1.471 -1.992 0.810 -3.730

0.0388888888888889 -2.858 2.052 -1.537 -2.000 0.815 -3.730

0.0333333333333333 -2.898 2.131 -1.601 -2.007 0.820 -3.730

0.0277777777777778 -2.937 2.207 -1.662 -2.013 0.824 -3.730

0.0222222222222222 -2.978 2.287 -1.727 -2.020 0.829 -3.731

0.0166666666666667 -3.017 2.363 -1.788 -2.027 0.834 -3.730

0.0111111111111111 -3.050 2.456 -1.874 -2.037 0.839 -3.733

0.00555555555555556 -3.079 2.556 -1.974 -2.049 0.845 -3.737

0 -3.100 2.658 -2.074 -2.061 0.851 -3.745