#Parameters

p <- .3 # the probability of a success

#Generating 10 random values

rbinom(10, size=1, prob=p) [1] 0 1 1 0 0 1 0 1 0 0Like the flip of a fair or unfair coin. X=1 if the coin comes up heads, 0 on tails.

#Parameters

p <- .3 # the probability of a success

#Generating 10 random values

rbinom(10, size=1, prob=p) [1] 0 1 1 0 0 1 0 1 0 0Expected value is \[\sum_k k\cdot Pr[X=k]\]

#All possible values

k <- 0:1

#Associated probabilities

Pr <- dbinom(k, size=1, prob=p)

#expectation

sum(k*Pr)[1] 0.3The expected value is \(p\) and the variance is \(p(1-p)\)

bernoulli.sim <- rbinom(100, size=1, prob=p)

# Expectation

p[1] 0.3# from sample

mean(bernoulli.sim)[1] 0.29# Variance

p*(1-p)[1] 0.21#from sample

var(bernoulli.sim)[1] 0.2079798Like flipping a fair (or unfair) coin \(n\) times, counting the number of heads.

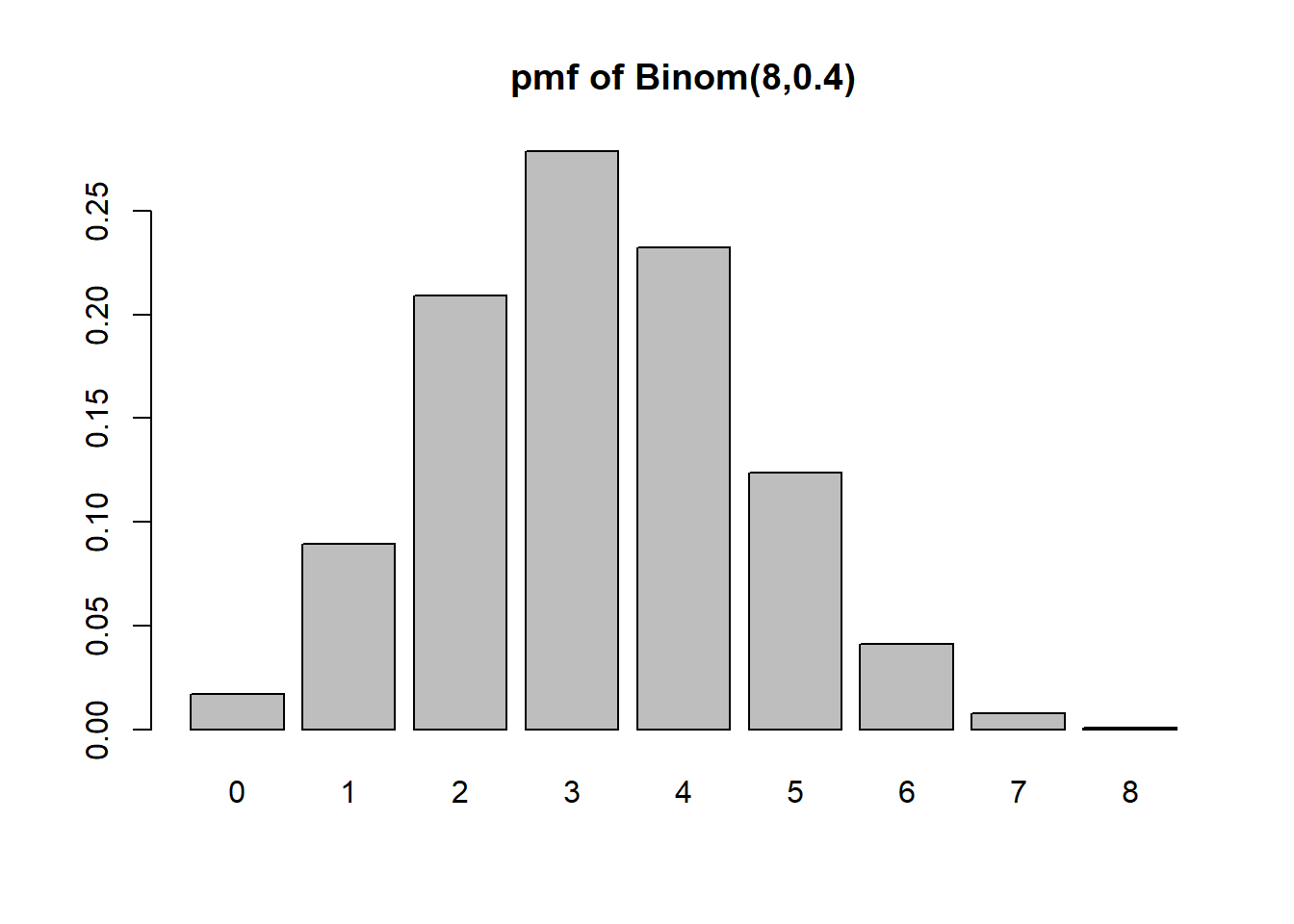

#Parameters

n <- 8 #the number of flips / attempts

p <- .4 #the probability of success

#Generate 10 random values

rbinom(10, size=n, prob=p) [1] 2 3 5 2 3 4 4 1 3 4#Calculate P(X=3)

dbinom(x=3, size=n, prob=p)[1] 0.2786918choose(n, 3)*p^3*(1-p)^(n-3)[1] 0.2786918#Calculate all probabilities

dbinom(x=0:8, size=n, prob=p)[1] 0.01679616 0.08957952 0.20901888 0.27869184 0.23224320 0.12386304 0.04128768

[8] 0.00786432 0.00065536sum(dbinom(x=0:8, size=n, prob=p))[1] 1#Calculate P(X <= 3)

pbinom(q=3, size=n, prob=p)[1] 0.5940864Visualize the binomial probability mass function:

k <- 0:8

pk <- dbinom(x=0:8, size=n, prob=p)

barplot(height=pk, names=k, main=paste0("pmf of Binom(",n,",",p,")"))

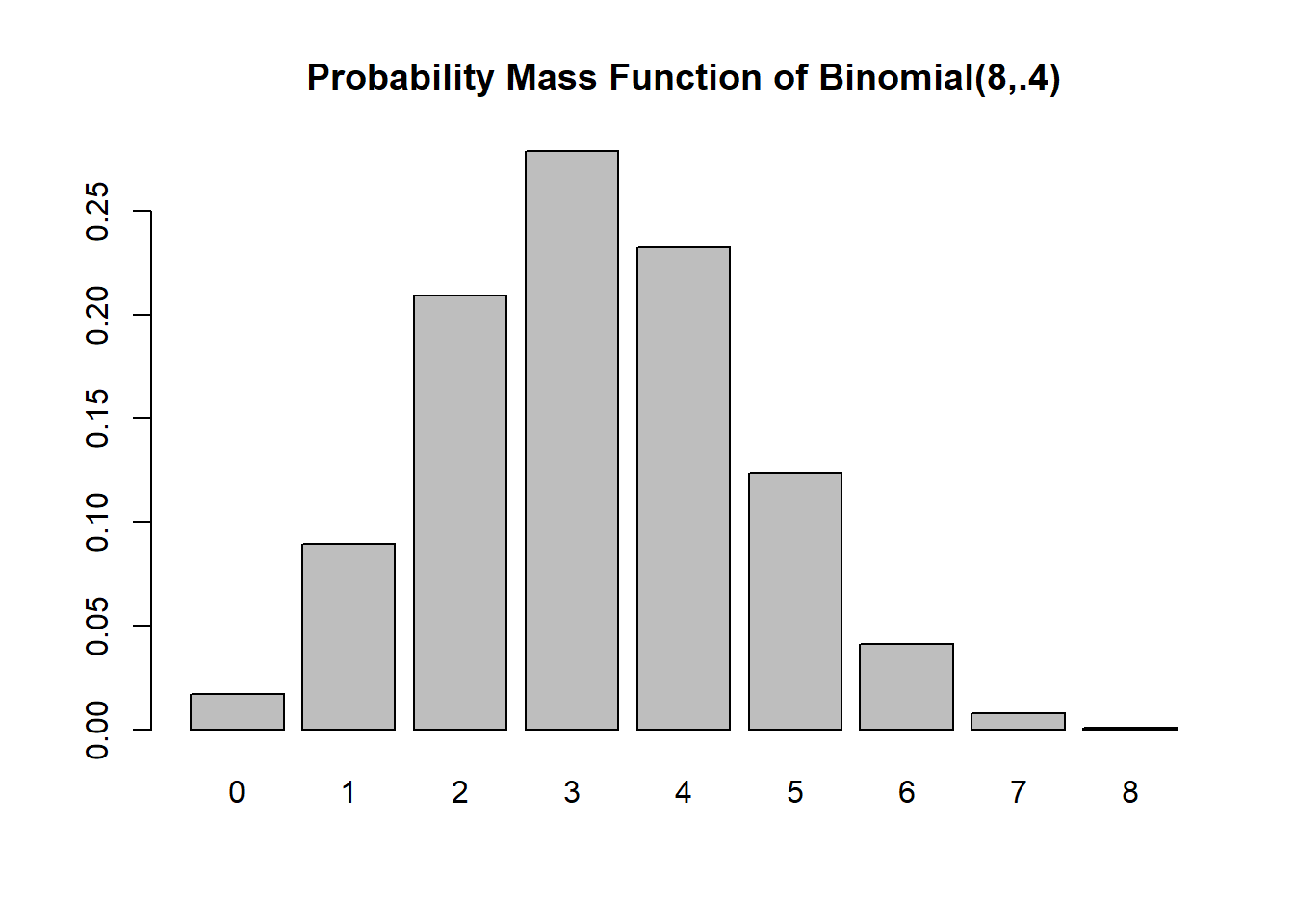

Expected value is \[\sum_k k\cdot Pr[X=k]\]

#All possible values

k <- 0:n

#Associated probabilities

Pr <- dbinom(k, size=n, prob=p)

#expectation

sum(k*Pr)[1] 3.2n*p[1] 3.2The probability mass function

barplot(Pr, names=k, main="Probability Mass Function of Binomial(8,.4)")

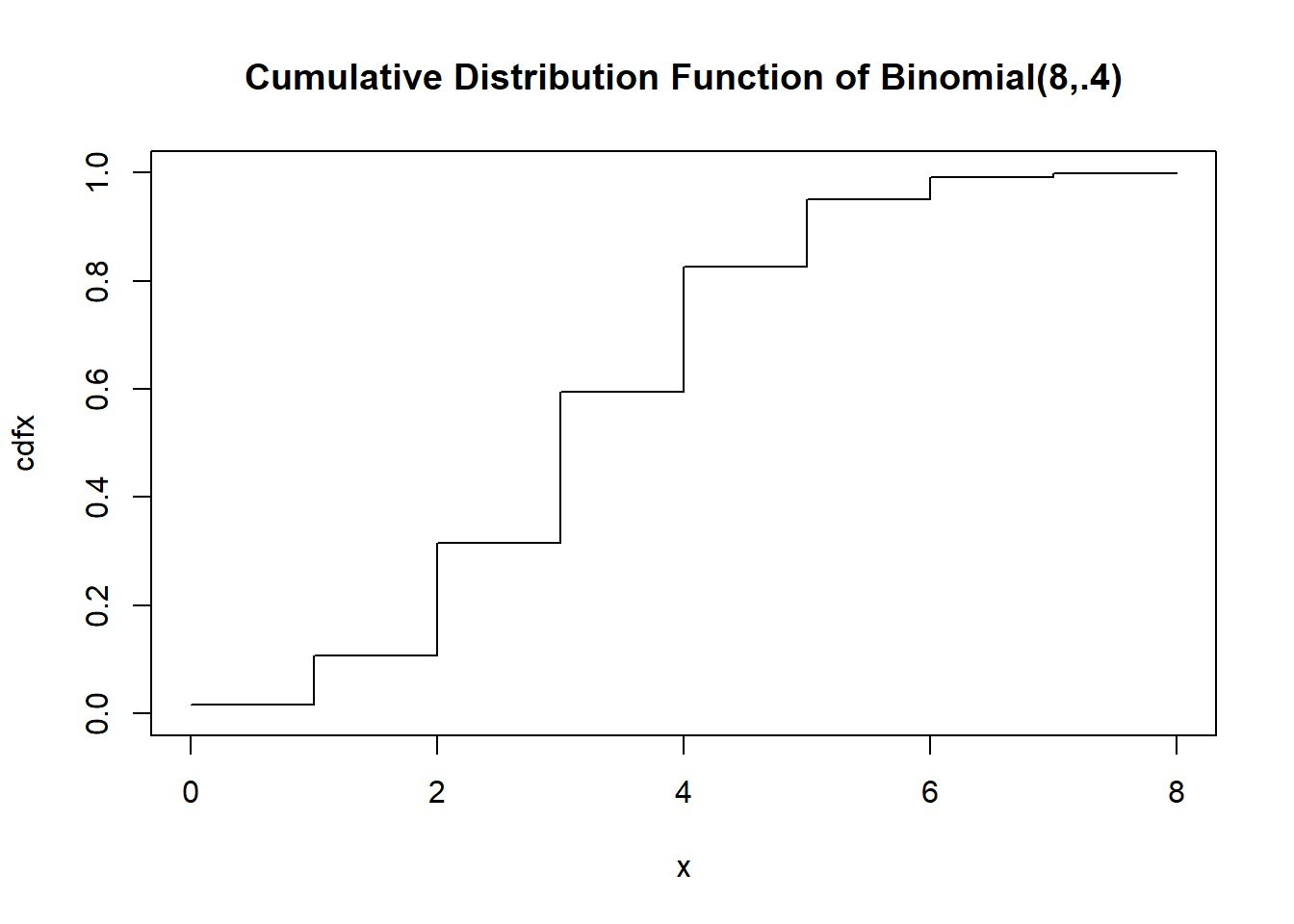

The cumulative distribution function

x <- 0:8

cdfx <- pbinom(x, size=n,prob=.4)

plot(x, cdfx, type="s", main="Cumulative Distribution Function of Binomial(8,.4)", ylim=c(0,1))

The expected value is \(np\) and the variance is \(np(1-p)\)

binomial.sim <- rbinom(10000, size=n, prob=p)

# Expectation

n*p[1] 3.2# from sample

mean(binomial.sim)[1] 3.2038# Variance

n*p*(1-p)[1] 1.92#from sample

var(binomial.sim)[1] 1.899255Counting how many tails before the first head; the number of failures before the first success (independent trials, probability of success remains constant)

#Parameters

p <- .4 #The probability of success on each trial

#Generate 10 random values

rgeom(10, prob=p) [1] 2 2 1 0 2 1 3 1 2 1The probability mass function…. only going out to 20, but the support is infinite!

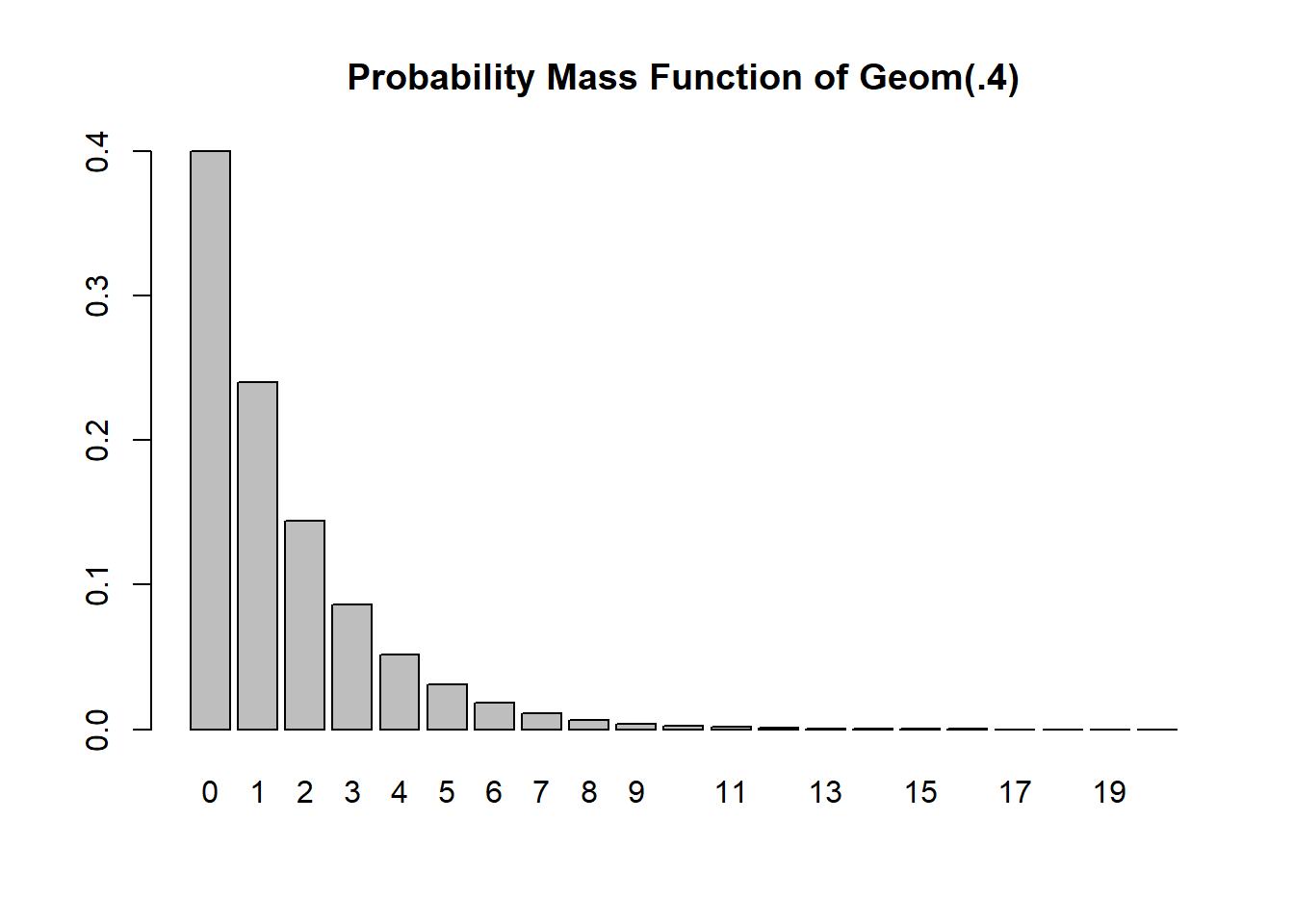

k <- 0:20

Pr <- dgeom(k, prob=p)

barplot(Pr, names=k, main="Probability Mass Function of Geom(.4)")

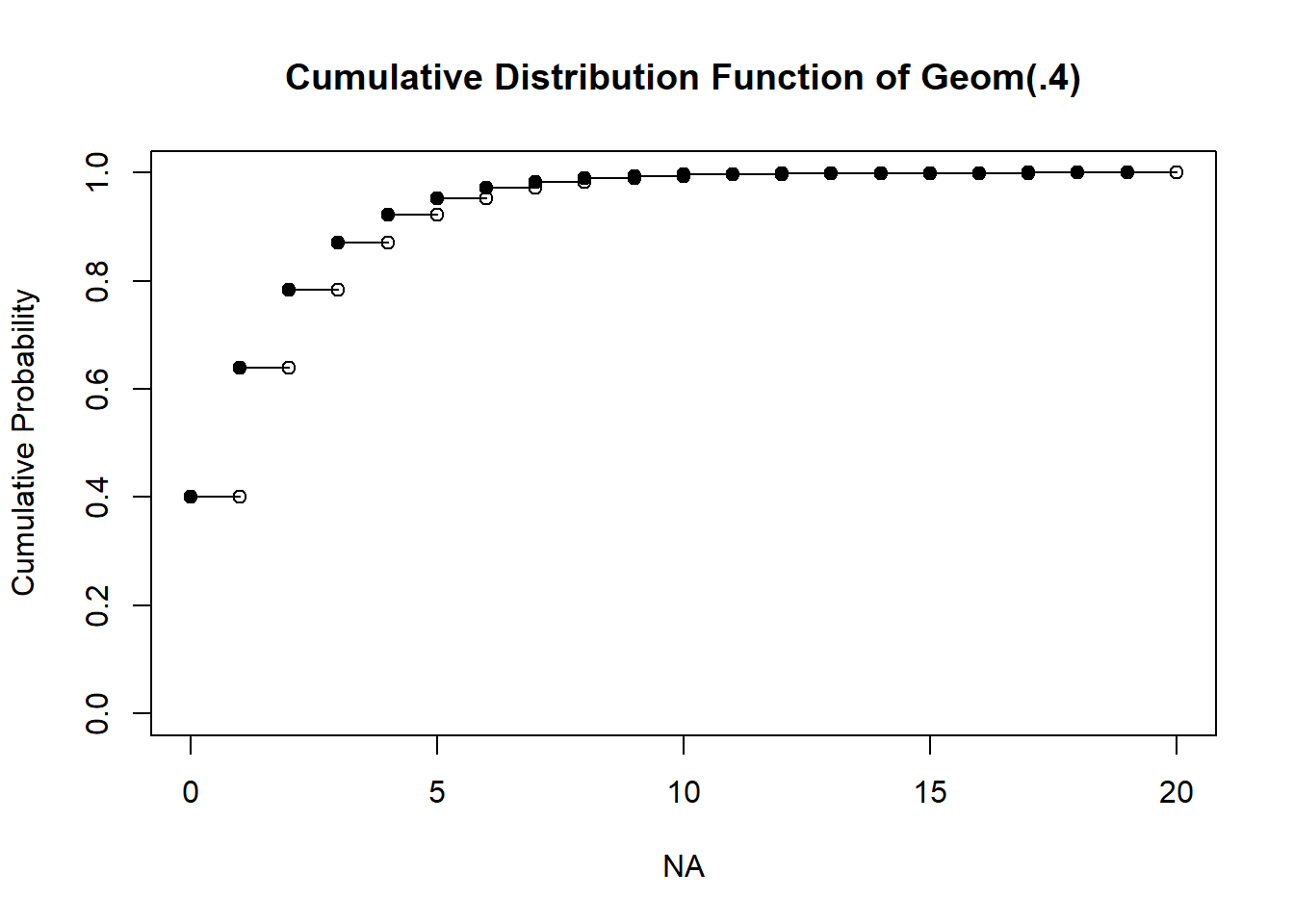

The cumulative distribution function

cdfx <- cumsum(Pr)

# if you want it to look really proper

n <- length(k)

plot(x = NA, y = NA, pch = NA,

xlim = c(0, max(k)),

ylim = c(0, 1),

ylab = "Cumulative Probability",

main = "Cumulative Distribution Function of Geom(.4)")

points(x = k[-n], y = cdfx[-n], pch=19)

points(x = k[-1], y = cdfx[-n], pch=1)

for(i in 1:(n-1)) points(x=k[i+0:1], y=cdfx[c(i,i)], type="l")

To calculate probabilities from a geometric rv, use the pgeom function

#Pr(X <= 3)

pgeom(3, prob=p)[1] 0.8704To get individual probabilities at k

#Pr(X=3)

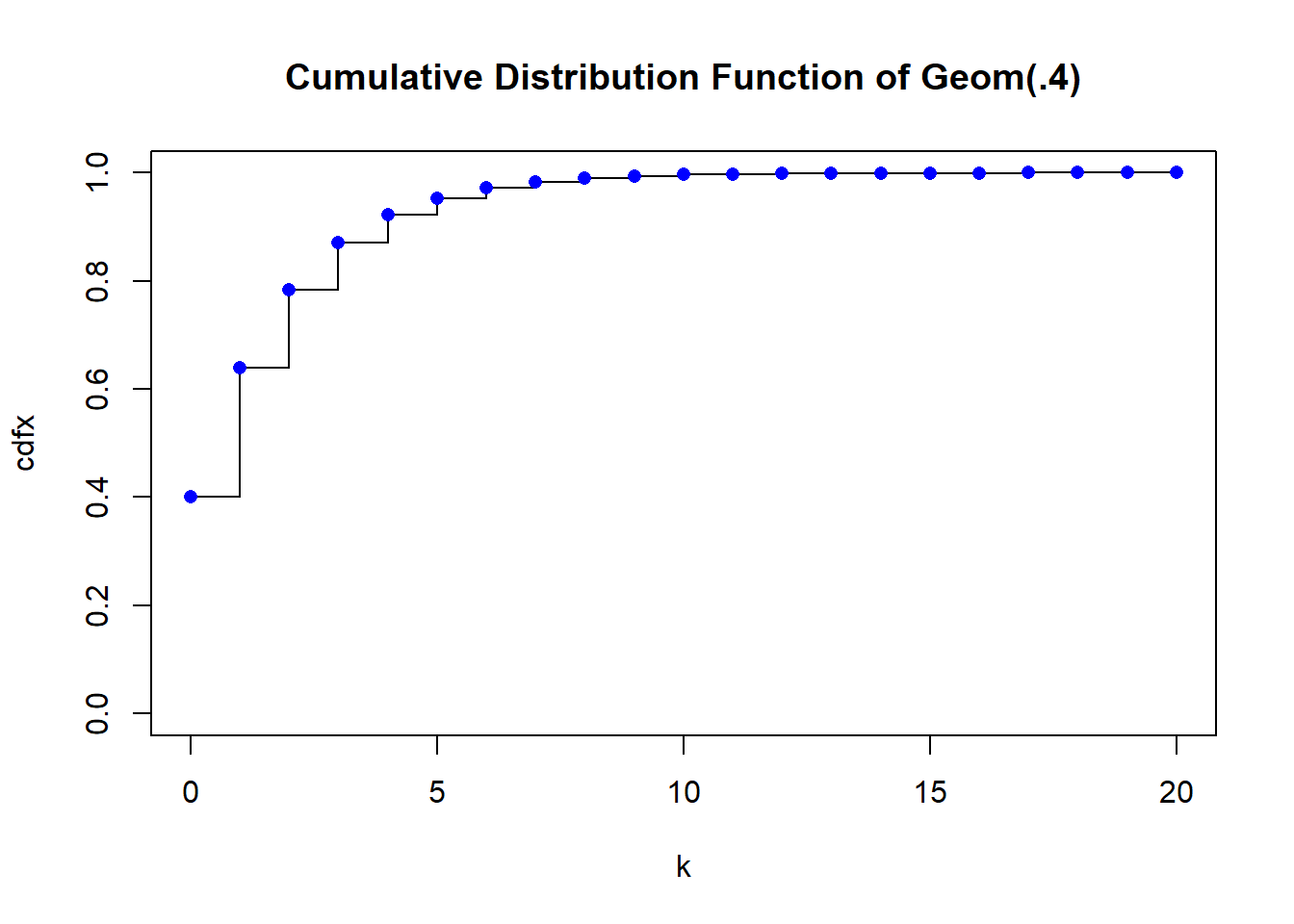

dgeom(3, prob=p)[1] 0.0864But it’s probably faster to just use a step type plot. The vertical lines are not technically part of the plot though.

plot(k, cdfx, type="s", main="Cumulative Distribution Function of Geom(.4)", ylim=c(0,1))

points(k, cdfx, pch = 16, col = "blue")

You can get the cumulative probabilities from the pgeom function

plot(k, pgeom(k, prob=.4), type="s", main="Cumulative Distribution Function of Geom(.4)", ylim=c(0,1))

points(k, cdfx, pch = 16, col = "blue")

The expected value is \(\dfrac{1-p}{p}\) and the variance is \(\dfrac{1-p}{p^2}\)

geom.sim <- rgeom(10000, prob=p)

# Expectation

(1-p)/p[1] 1.5# from sample

mean(geom.sim)[1] 1.5059# Variance

(1-p)/(p^2)[1] 3.75#from sample

var(geom.sim)[1] 3.826348Like the number of times something occurs during a fixed time window

#Parameters

l <- 10.5 #The rate parameter, average occurrences per unit time

#It is lambda, but I'll call it "l"

#Generate 10 random values

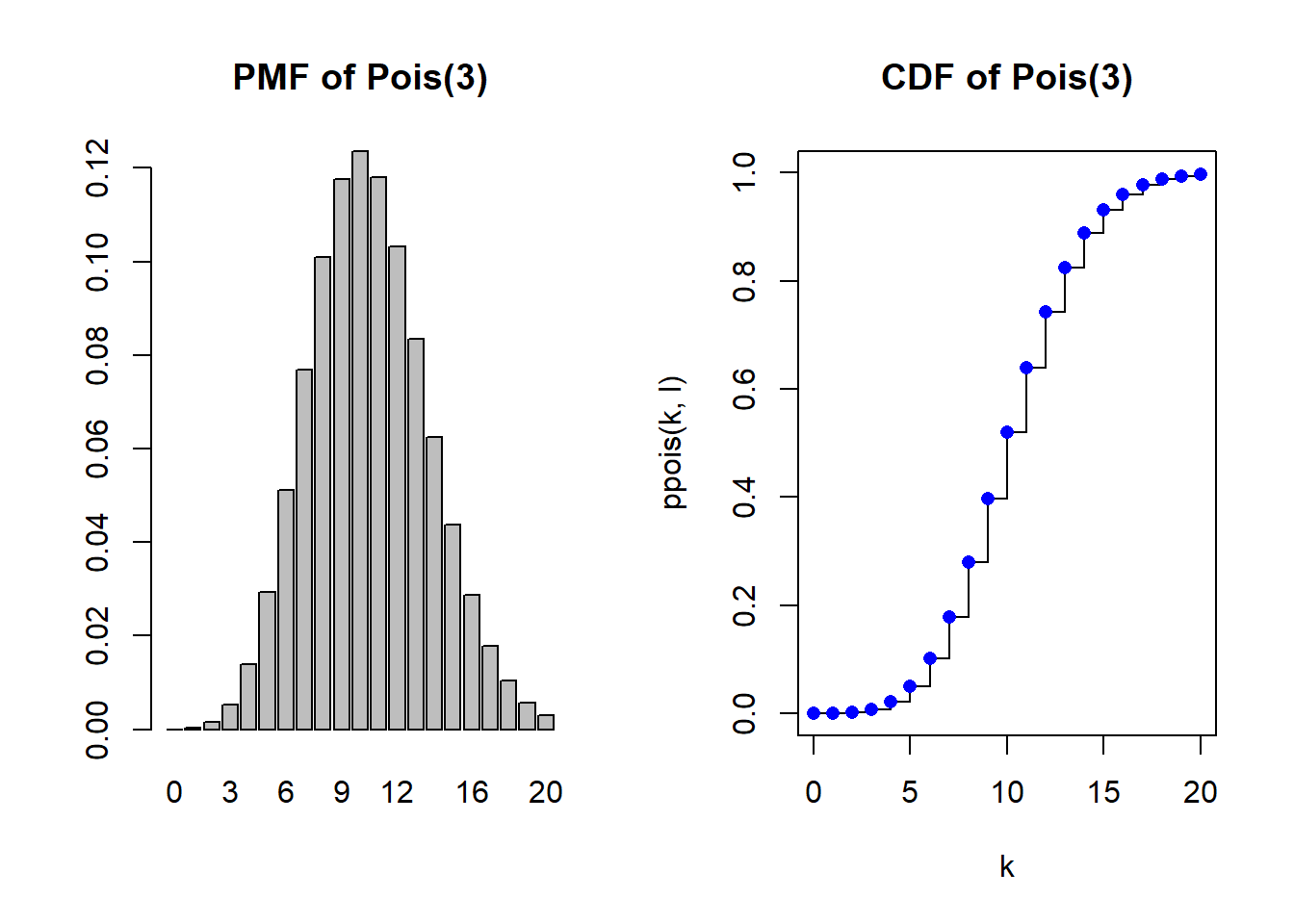

rpois(10, lambda=l) [1] 4 12 13 12 10 10 8 9 9 10PMF and CDF

par(mfrow=c(1,2))

k <- 0:20

Pr <- dpois(k,l)

barplot(Pr, names=k, main="PMF of Pois(3)")

plot(k, ppois(k, l), type="s", main="CDF of Pois(3)", ylim=c(0,1))

points(k, ppois(k, l), pch = 16, col = "blue")

The expected value and variance are both is \(\lambda\)

pois.sim <- rpois(10000, lambda=l)

# Expectation & Variance

l[1] 10.5# mean from sample

mean(pois.sim)[1] 10.4465#variance from sample

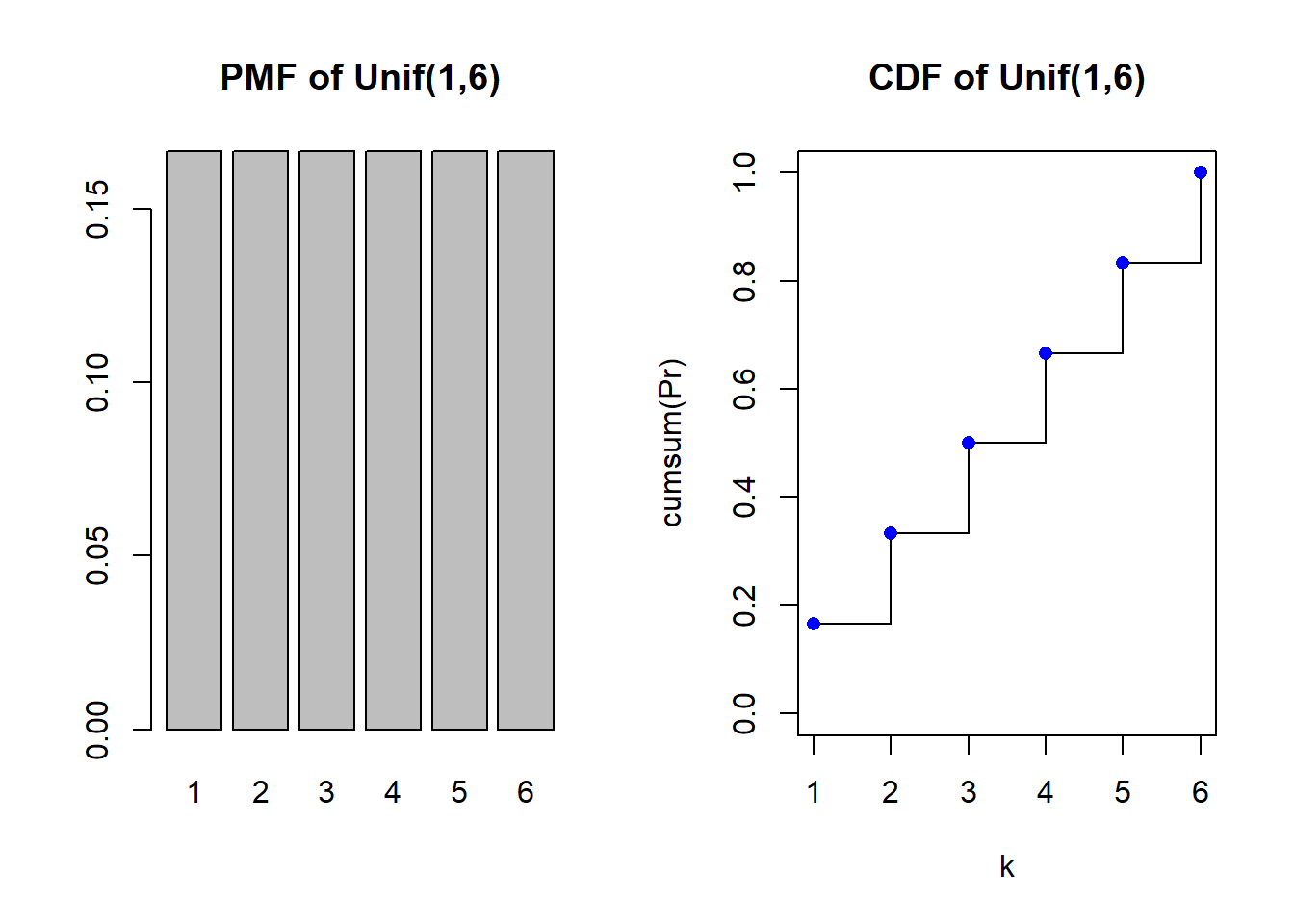

var(pois.sim)[1] 10.47599Like rolling a fair die

#Parameters

a <- 1 #lower bound, inclusive

b <- 6 #upper bound, inclusive

#Generate 10 random values

sample(a:b, 10, replace=TRUE) #replace=TRUE is important [1] 4 3 5 4 5 5 3 2 3 6The PMF and CDF

par(mfrow=c(1,2))

k <- a:b

Pr <- rep(1/(b-a+1), length(k))

barplot(Pr, names=k, main="PMF of Unif(1,6)")

plot(k, cumsum(Pr), type="s", main="CDF of Unif(1,6)", ylim=c(0,1))

points(k, cumsum(Pr), pch = 16, col = "blue")

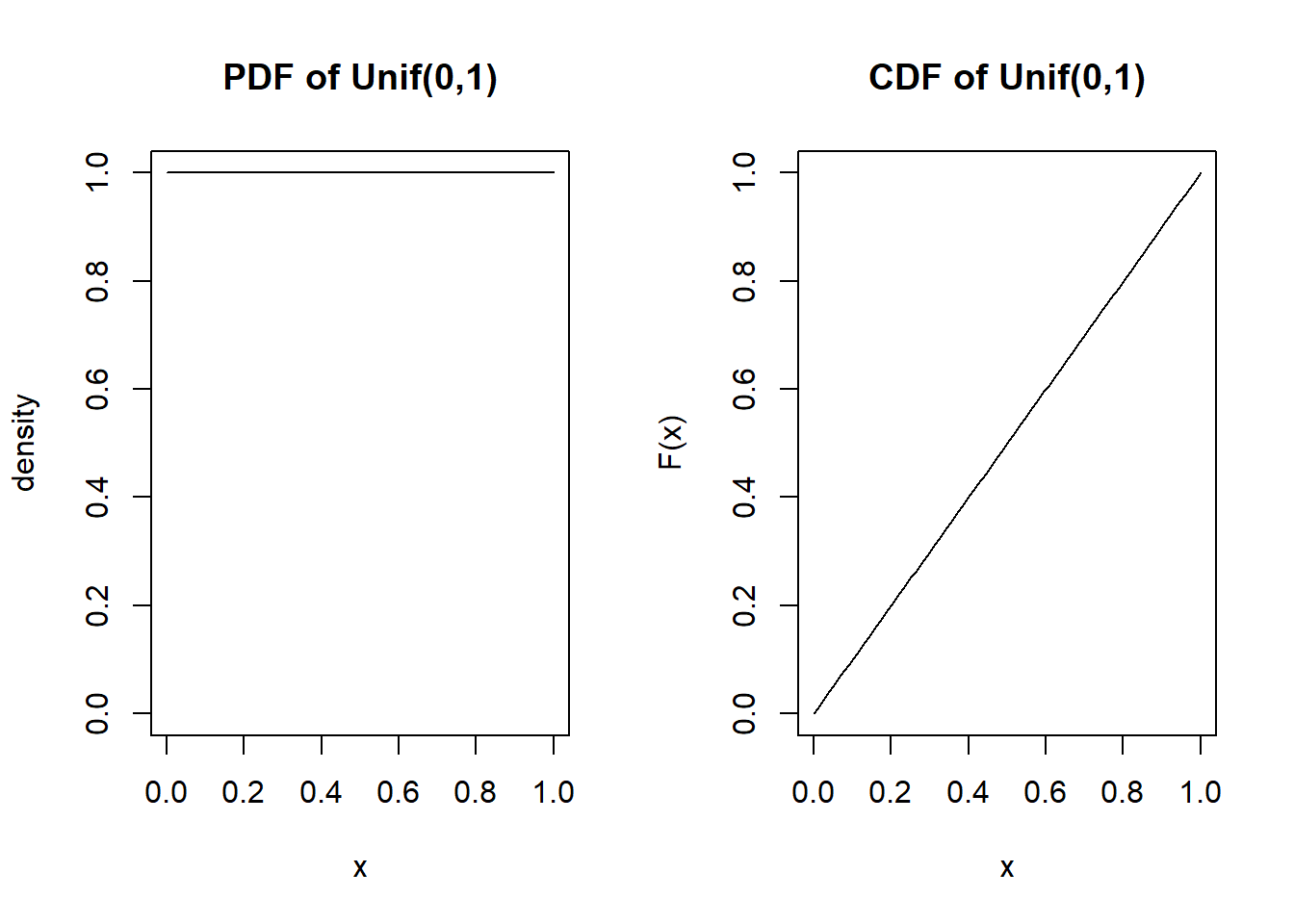

The backbone of random variable generation - for example a random decimal between 0 and 1

# Parameters

a <- 0 #lower bound

b <- 1 #upper bound

#generate 10 random values

runif(10, min=a, max=b) [1] 0.2953279 0.3762149 0.9997242 0.7867803 0.8583449 0.5822392 0.2107988

[8] 0.7183277 0.8639896 0.4345879Probability density function and cumulative distribution function

par(mfrow=c(1,2))

x <- seq(a,b, length.out=100)

plot(x, dunif(x, a, b), type="l", main="PDF of Unif(0,1)", ylab="density", ylim=c(0,1))

plot(x, punif(x, a, b), type="l", main="CDF of Unif(0,1)", ylab="F(x)")

The expected value is \(\frac{a+b}{2}\) and the variance is \(\frac{(b-a)^2}{12}\)

unif.sim <- runif(10000, min=a, max=b)

# Expectation

(a+b)/2[1] 0.5# mean from sample

mean(unif.sim)[1] 0.4993472#variance

(b-a)^2/12[1] 0.08333333#variance from sample

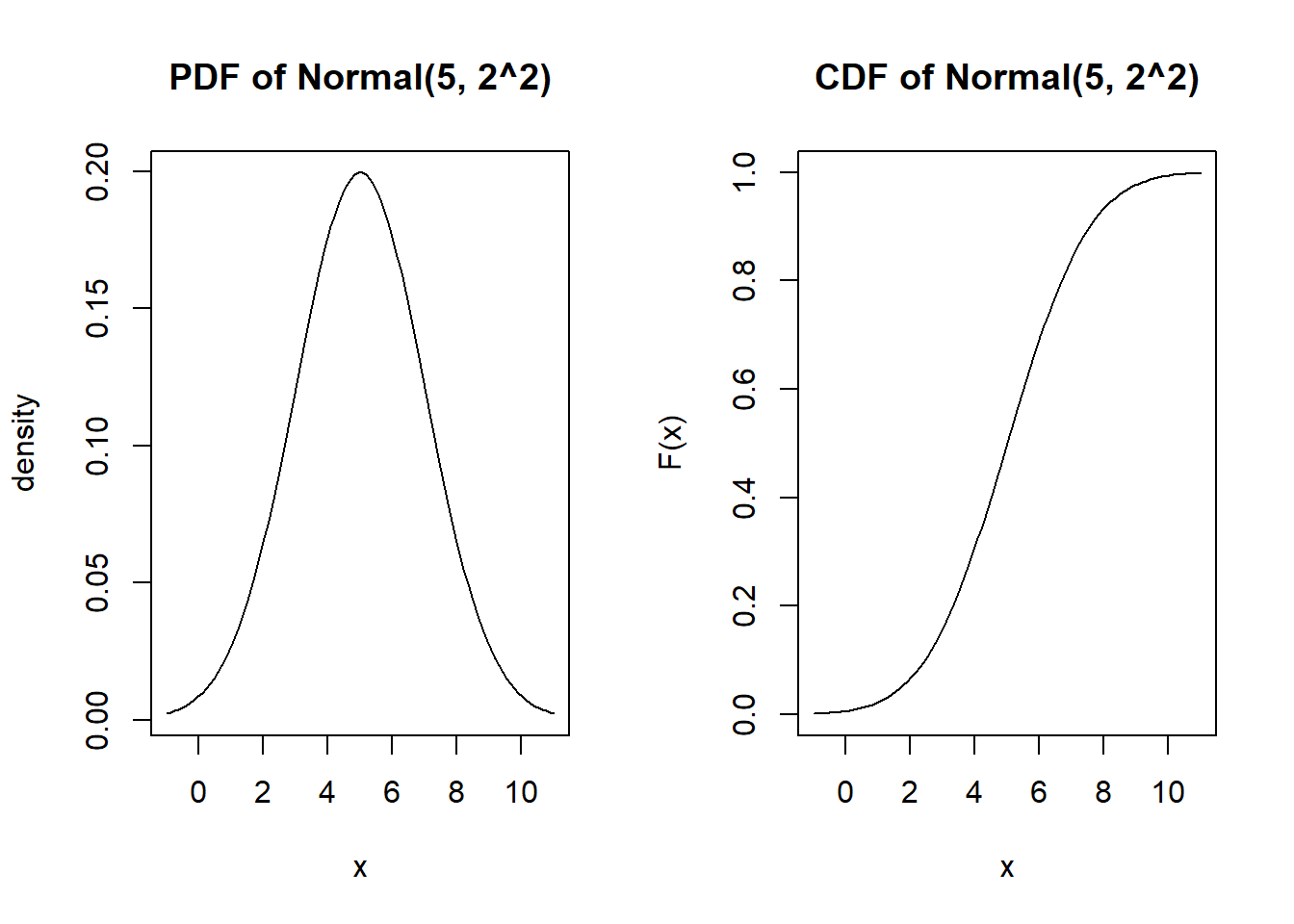

var(unif.sim)[1] 0.08349469Many things in the world are normally distributed - useful for modeling when the distribution is symmetric and probability is densest in the middle with decreasing tails.

#Parameters

mu <- 5 #the mean/location of the distribution

sigma2 <- 4 #the variance is in squared units!!

sigma <- sqrt(sigma2) #sigma is the standard deviation, not the variance

#generate 10 random values

rnorm(10, mean=mu, sd=sigma) [1] 5.7379241 5.7693920 6.0246647 3.1971162 1.4964911 5.8024497 5.5295972

[8] 0.5755244 4.5957016 3.2427507Probability density function and cumulative distribution function

par(mfrow=c(1,2))

x <- seq(mu-3*sigma, mu+3*sigma, length.out=100)

plot(x, dnorm(x, mu, sigma), type="l", main="PDF of Normal(5, 2^2)", ylab="density")

plot(x, pnorm(x, mu, sigma), type="l", main="CDF of Normal(5, 2^2)", ylab="F(x)")

Approximate the expected value numerically

\[\int_{-\infty}^\infty t f(t) dt\]

mu <- 15

sigma <- 4

t <- seq(mu-4*sigma, mu+4*sigma, length.out=1000)

d <- dnorm(t, mean=mu, sd=sigma)

w <- t[2]-t[1]

head(t)[1] -1.0000000 -0.9679680 -0.9359359 -0.9039039 -0.8718719 -0.8398398head(d)[1] 3.345756e-05 3.454551e-05 3.566656e-05 3.682162e-05 3.801165e-05

[6] 3.923763e-05#Expected value

sum( t * (d*w))[1] 14.99907The expected value is \(\mu\) and the variance is \(\sigma^2\)

normal.sim <- rnorm(10000, mean=mu, sd=sigma)

# Expectation

mu[1] 15# mean from sample

mean(normal.sim)[1] 15.01916#variance

sigma2[1] 4#variance from sample

var(normal.sim)[1] 16.03533normal.sim <- rnorm(1000000)

x <- .25 <= normal.sim & normal.sim <=.75

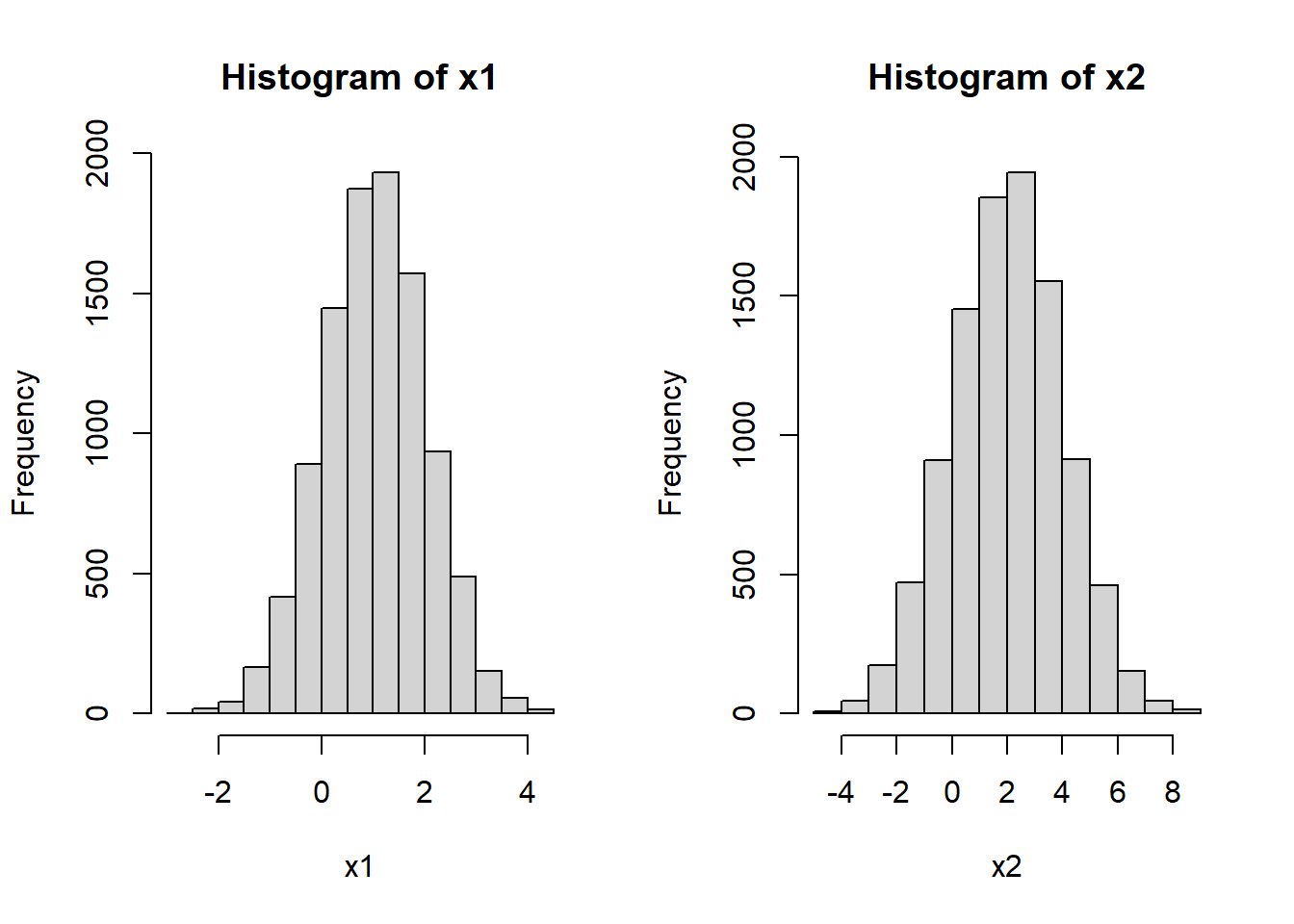

sum(x)/1000000[1] 0.174265pnorm(.75)-pnorm(.25)[1] 0.1746663# X1 ~ Normal(1,1^2)

x1 <- rnorm(10000, mean=1, sd=1)

#X2 ~ Normal(2, 2^2)

x2 <- rnorm(10000, mean=2, sd=2)

par(mfrow=c(1,2))

hist(x1)

hist(x2)

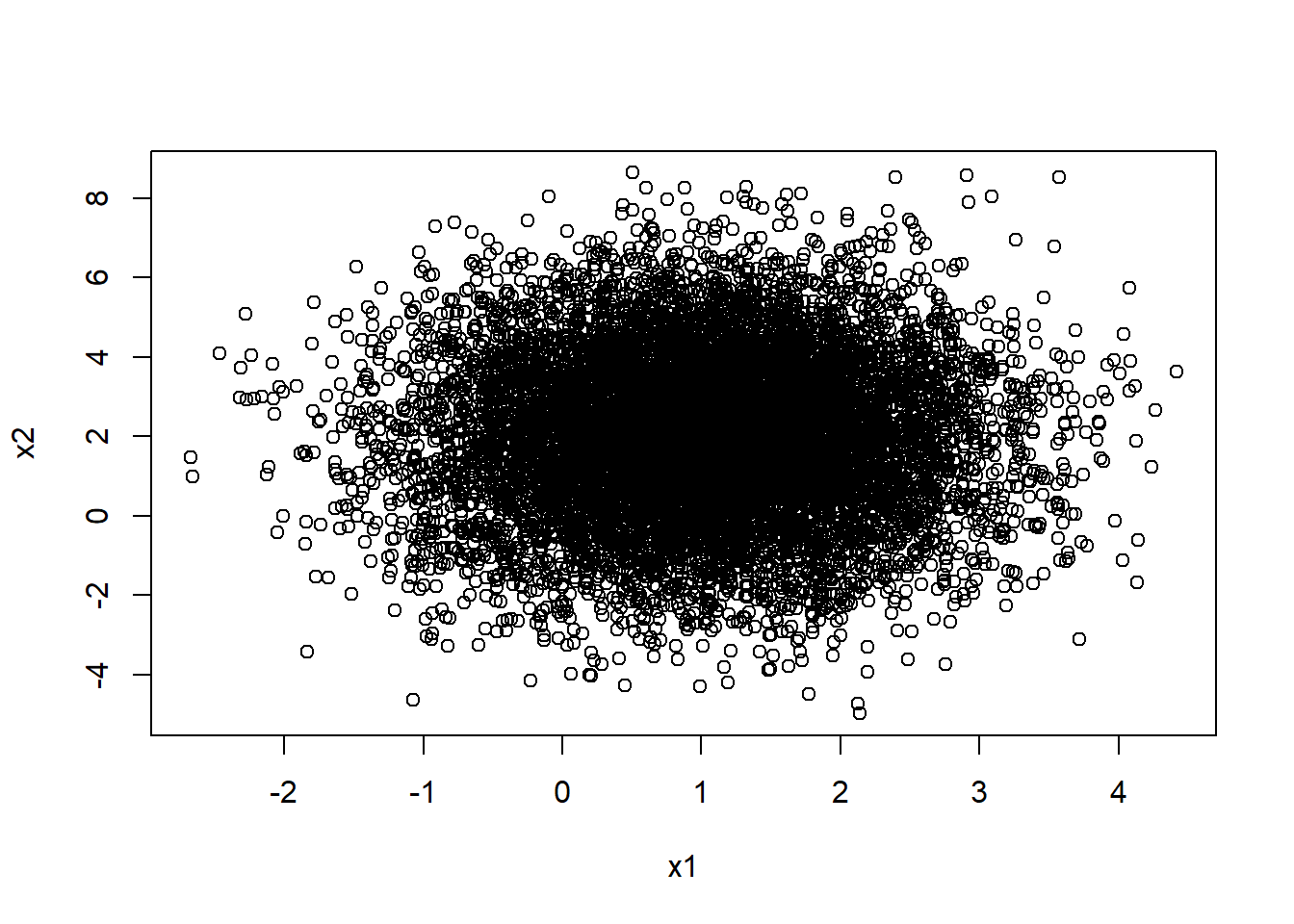

Let’s check the variances individually

var(x1)[1] 0.9965541var(x2)[1] 3.944507In theory, Var(X1+X2) = Var(X1) + Var(X2) We check with sample variance

var(x1+x2)[1] 4.936043var(x1)+var(x2)[1] 4.941061var(x1)+var(x2)+2*cov(x1,x2)[1] 4.936043Look at the plot of these two variables

mean(x1+x2)[1] 3.016663mean(x1)+mean(x2)[1] 3.016663plot(x1,x2)

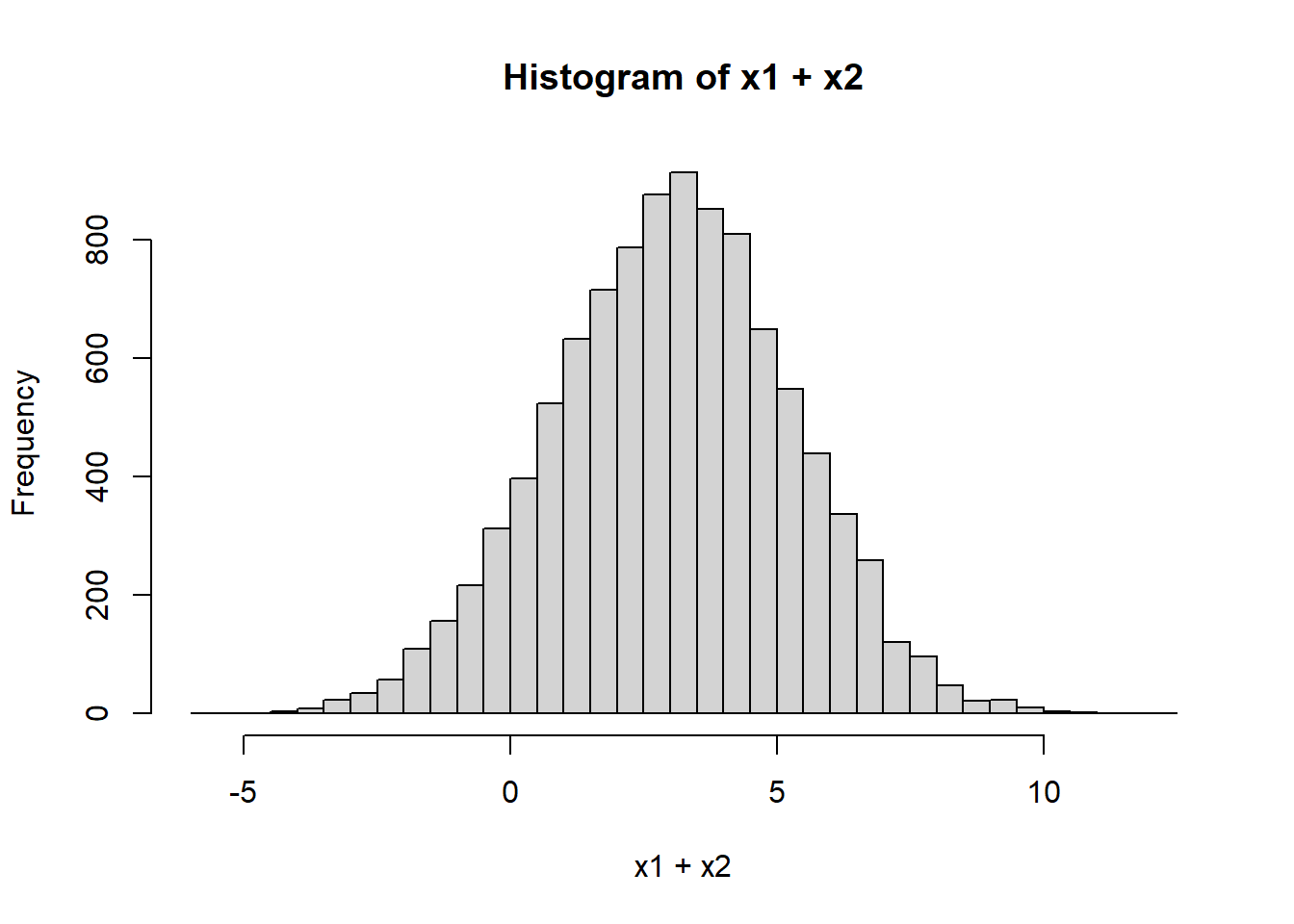

hist(x1+x2, breaks=50)

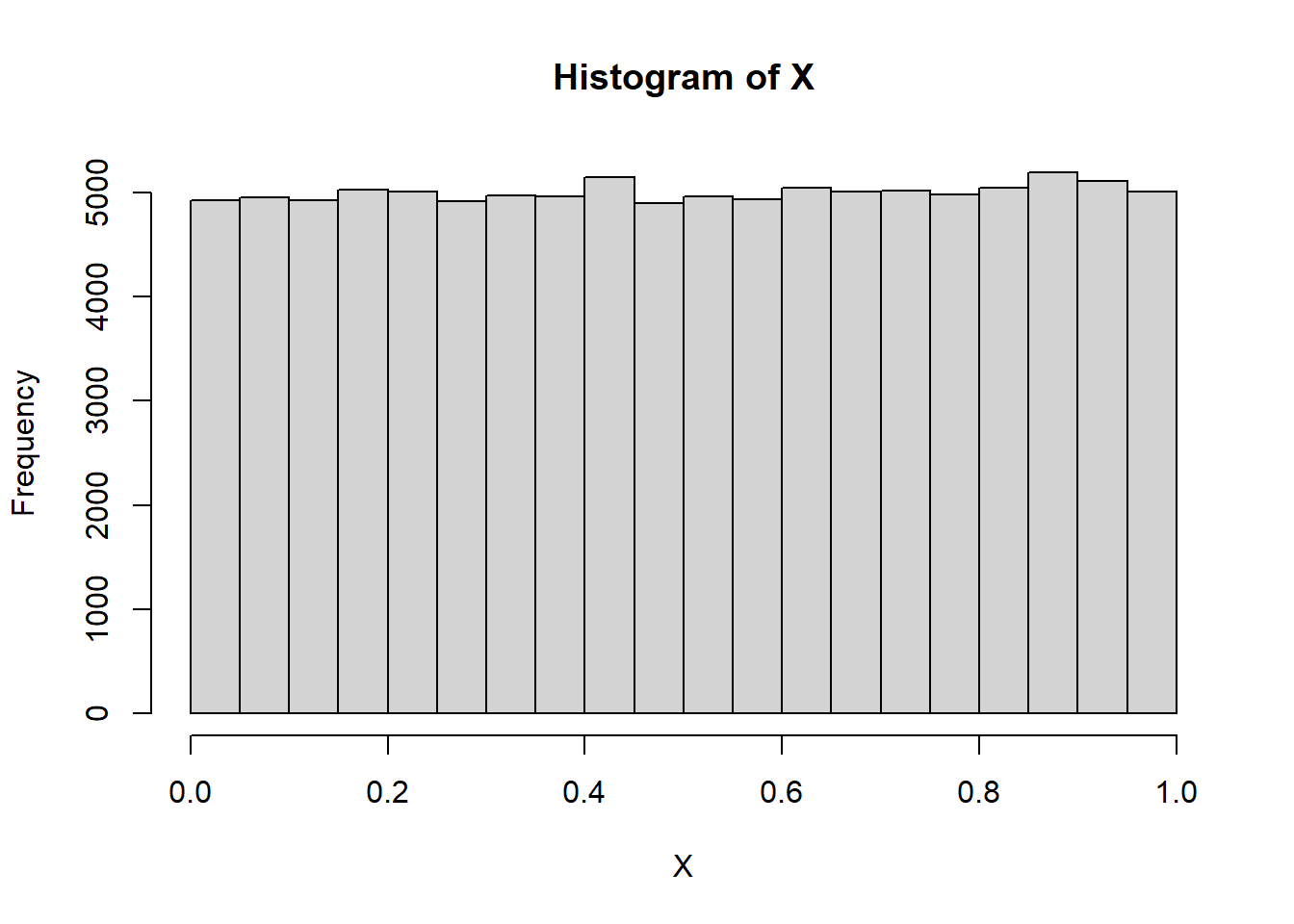

X <- runif(100000, 0, 1)

hist(X)

Y <- runif(100000, 0, 1)

hist(Y)

hist(X+Y)

Z <- runif(100000, 0, 1)

hist(X+Y+Z, breaks=100)

Let’s consider a geometric that counts the number of days before a electronic component malfunctions Suppose that every day there’s a 25% chance of malfunction.

p=.25

random.geom <- rgeom(10000, prob=p)

hist(random.geom, breaks=25)

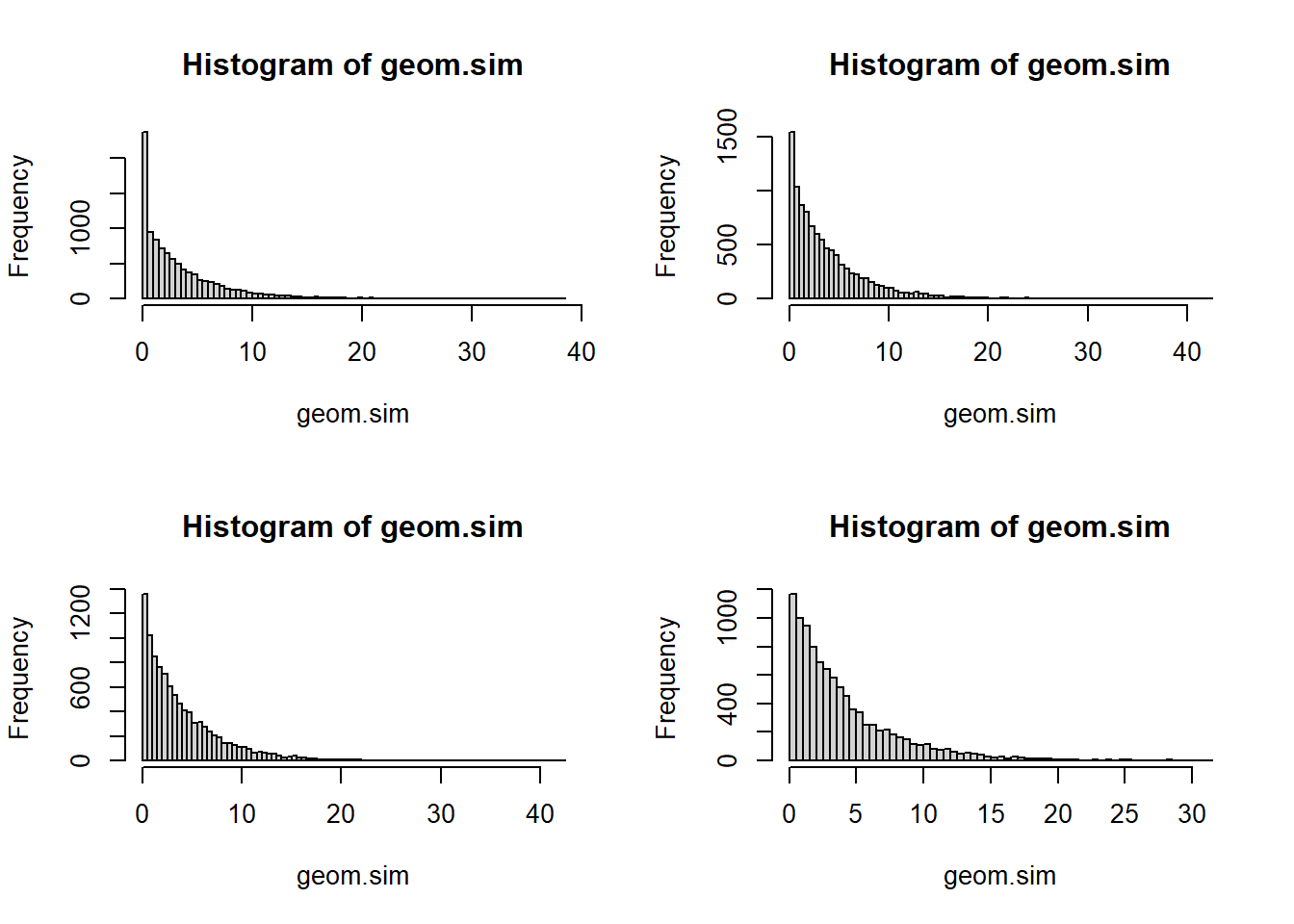

What if more than one malfunction could happen per day? Like we replace the part immediately when it malfunctions. We could divide the day into \(N\) parts and use a geometric for each part of the day. If \(X\)=k, then the proportion of the day it took to break is \(k/N\) Let’s start with \(N\)=2 and go up from there

par (mfrow=c(2,2))

N <- 2

geom.sim <- rgeom(10000, p/N) / N

hist(geom.sim, breaks=100)

mean(geom.sim)[1] 3.5007N <- 6

geom.sim <- rgeom(10000, p/N) / N

hist(geom.sim, breaks=100)

mean(geom.sim)[1] 3.915017N <- 24

geom.sim <- rgeom(10000, p/N) / N

hist(geom.sim, breaks=100)

mean(geom.sim)[1] 4.059958N <- 100

geom.sim <- rgeom(10000, p/N) / N

hist(geom.sim, breaks=100)

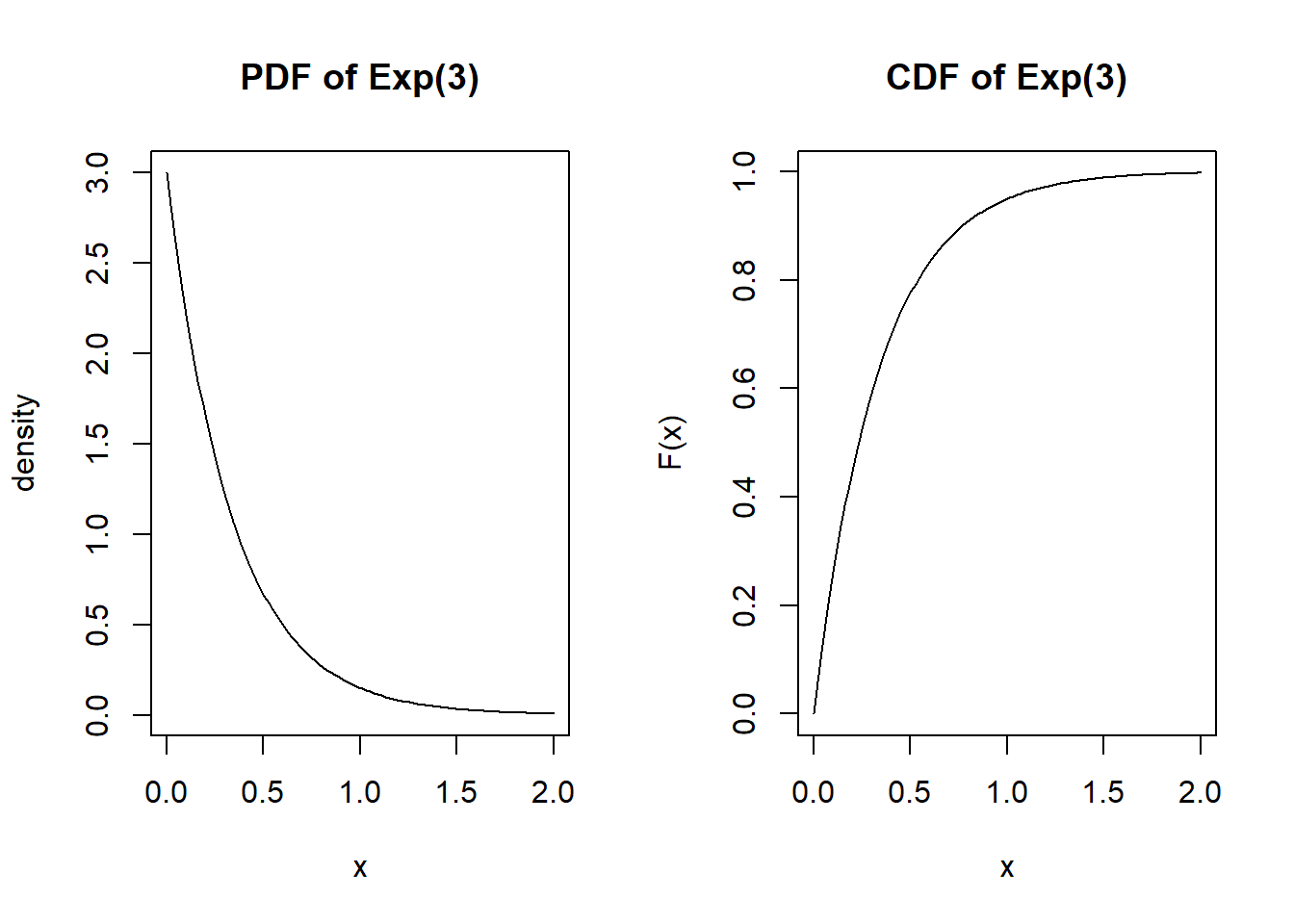

mean(geom.sim)[1] 3.990827For modeling waiting times - the length of time until an event occurs. It’s a continuous version of a geometric, if you start looking at smaller and smaller time units (e.g. days -> hours -> minutes -> seconds)

#Parameters

l <- 3 #The rate parameter, the average number of occurrences per unit time

#Generate 10 random values

rexp(10, rate=l) [1] 0.230439147 0.089207281 0.157374512 0.096684376 0.266710576 0.045621745

[7] 0.002265614 0.807557267 0.033897664 0.595115799Probability density function and cumulative distribution function

par(mfrow=c(1,2))

x <- seq(0, 6/l, length.out=100)

plot(x, dexp(x, l), type="l", main="PDF of Exp(3)", ylab="density")

plot(x, pexp(x, l), type="l", main="CDF of Exp(3)", ylab="F(x)")

The expected value is \(\dfrac{1}{\lambda}\) and the variance is \(\frac{1}{\lambda^2}\)

exp.sim <- rexp(10000, l)

# Expectation

1/l[1] 0.3333333# mean from sample

mean(exp.sim)[1] 0.3287313#variance

1/l^2[1] 0.1111111#variance from sample

var(exp.sim)[1] 0.1060149If rate = 1, what is \(Pr(X < 5)\)

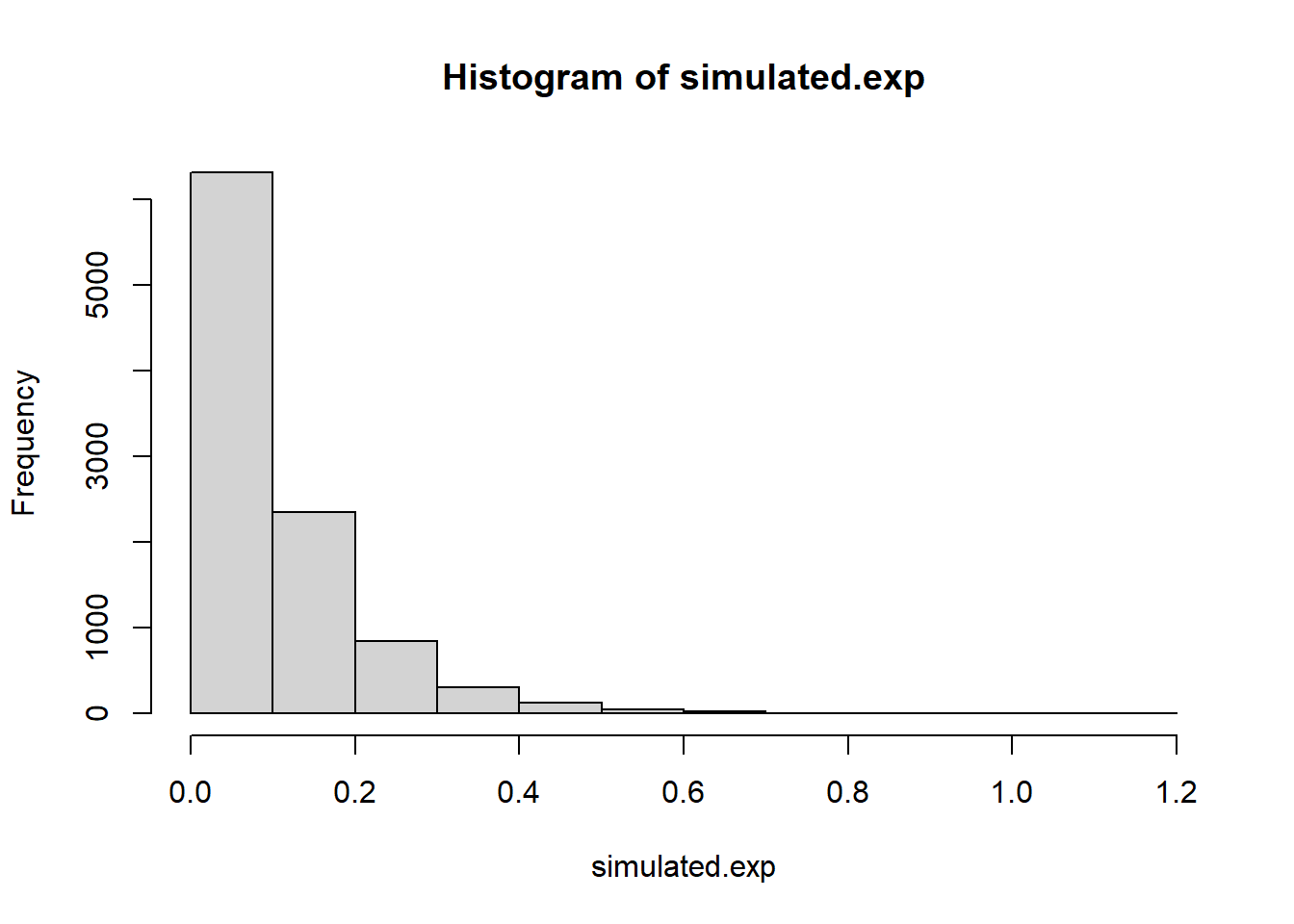

pexp(5, rate=1)[1] 0.9932621lambda = 10

simulated.exp <- rexp(10000, rate=10)

hist(simulated.exp)

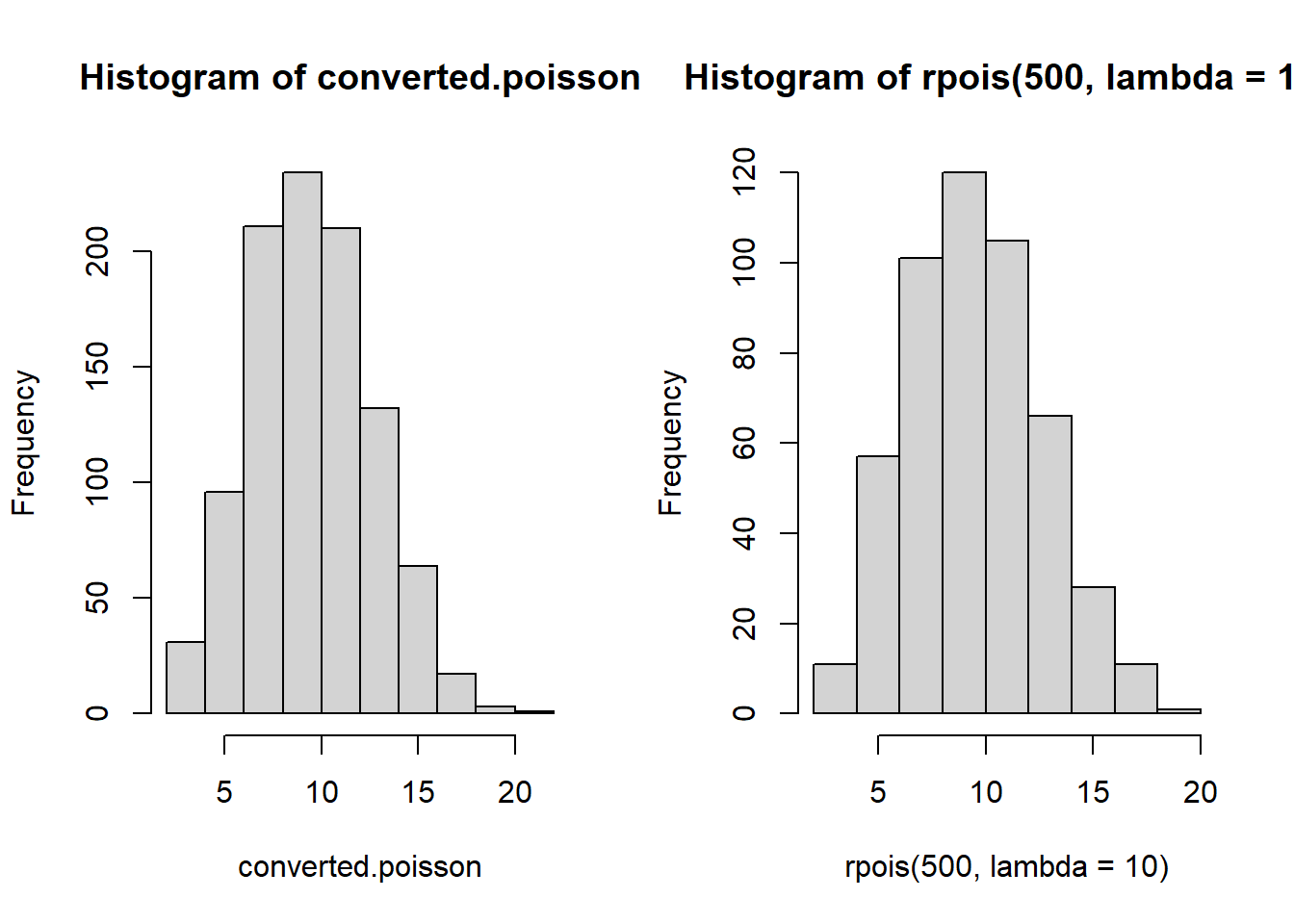

head(simulated.exp)[1] 0.22583907 0.10158912 0.15125233 0.05763004 0.22733971 0.21002218converted.poisson <- as.vector(table(floor(cumsum(simulated.exp))))

par(mfrow=c(1,2))

hist(converted.poisson)

hist(rpois(500, lambda=10))

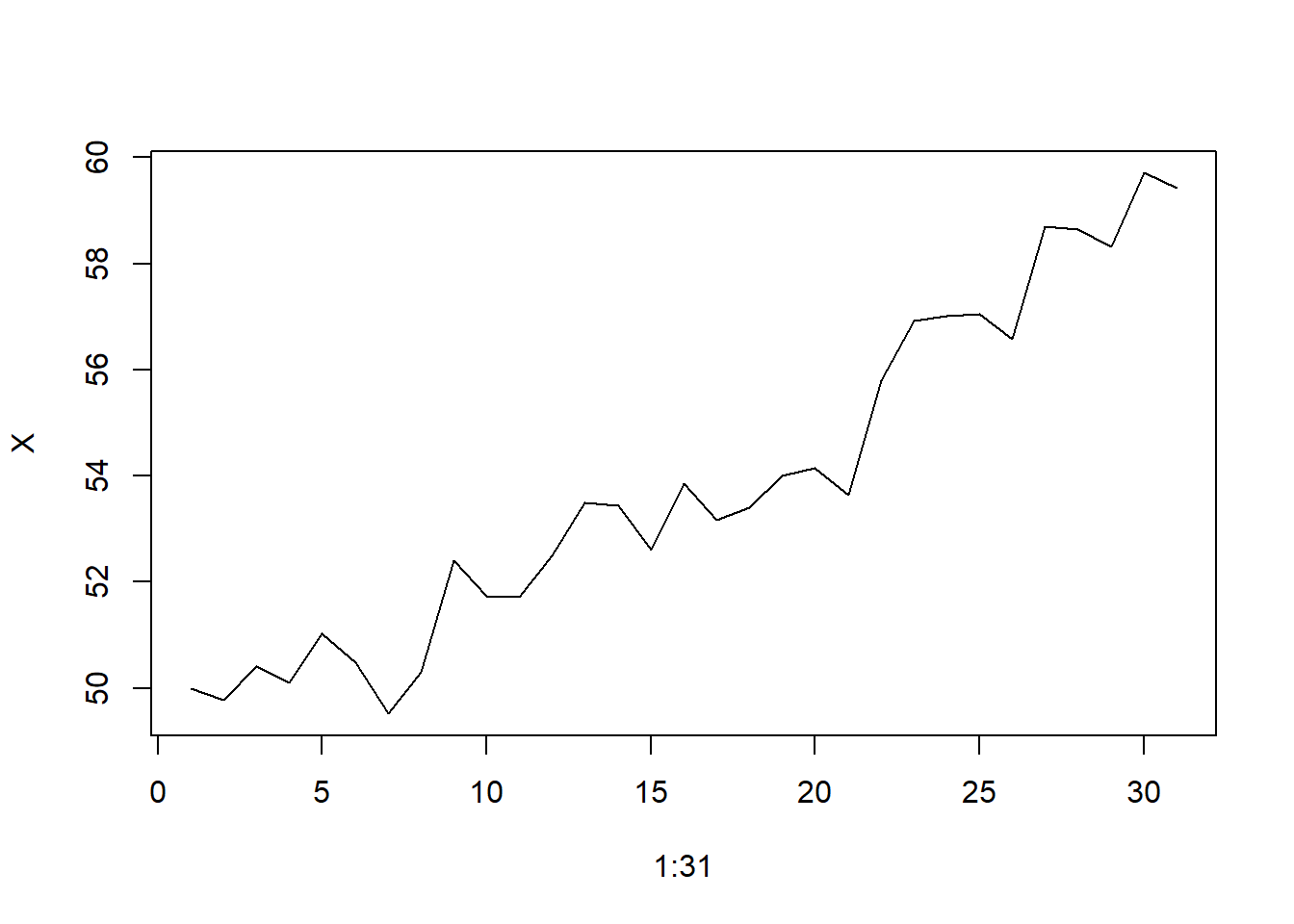

Here’s an example of how you could combine normally distributed random variables for a model of daily stock prices. This is an example of a random walk.

deltas <- rnorm(30)

X <- 50 + c(0,cumsum(deltas))

plot(x=1:31, y=X, type="l")